International Journal of Management Science and Business Administration

Volume 6, Issue 6, September 2020, Pages 41-50

An Analysis of Romanian Capital, Forex and Monetary Markets: Volatilities and Contagion

DOI: 10.18775/ijmsba.1849-5664-5419.2014.66.1004

URL: http://dx.doi.org/10.18775/ijmsba.1849-5664-5419.2014.66.1004

Carmen Emilia Pascal

Academy of Economic Studies, Faculty of Finance, Insurance, Banking and Stock Exchange,

Bucharest, Romania

Abstract: This paper focuses on stability relations for the Romanian main financial markets: capital, ForEx and monetary markets, as well as the intensity of the link between them and how they are interconnected, because this represents the best indicator of the situation of an economy, which is seen as a complex, adaptive and dynamic system, that is continuously changing. This analysis examines their deviation from the state of equilibrium, and what are the factors that modify this state. The study incorporates the markets evolution, their estimated volatilities, it shows that the most sensitive to the impact of a financial shock are the currency and the stock market. All the obtained results are correlated with events, news and market information from those particular moments to find explanations and understand the behavior of investors and how their decisions affected the market. Because of instability on some markets, investors started moving their finances to other markets, where they had more confidence, causing imbalances. Behavior of investors, as they react to the emergence of a shock, is decisive and extremely important in anticipating the effects that such a financial shock can produce. The values of the estimated volatilities were embedded into a volatility table to be easier to track their evolution over the period under review (2007 – 2018). Besides the financial crisis, there have been other events that have translated into a higher degree of volatility: raising the minimum wage, the Brexit, protests against corruption, the raise of salaries for the public workers which has created instability in the monetary market. The analysis continues with an estimate of a spillover index that only confirms the significant vulnerability period in the markets: 2010-2012, period during which the phenomenon of contagion may have occurred.

Keywords: Capital market, Contagion, Foreign exchange market, GARCH, Spillover index

An Analysis of Romanian Capital, Forex and Monetary Markets: Volatilities and Contagion

1. Introduction

Volatility is inevitable. There are multiple factors that can lead to uncertainty in the markets: political events, such as strikes, changes in legislations, presidential elections, or major financial or social events like financial crises, wars or conflicts. As countries and economies are becoming more and more interconnected nowadays it also happens that events in one country could impact the markets in another country, through trading links, for example. The behaviour of investors, whether it is rational or irrational, allows shocks to take place from one country to another. Investors can follow irrational strategies according to their own preferences or the behaviour of other investors. For investors the safest option is to not react and not take decisions based on impulse in these situations of unpredictability. They should follow their risk appetite, respect their long-term plan and investment strategy and use diversification in order to reduce exposure to risk. It is considered that the gap between financial risk tolerance and emotional risk tolerance is the widest in such turbulent periods. An example of a factor that can generate turbulence on the stock market can come from the labour market. In their study on the impact of unemployment news on the stock market, Boyd, Hu and Jagannathan (2005), use the fact that this type of news has 3 information embedded: about future interest rates (information that dominates in expansion periods), about equity risk premium and information on corporate earnings and dividends (which dominates during economic contractions). They show that during expansions average stock prices and bond prices increase on bad news regarding unemployment, while during contractions stock prices decrease, but for the bond prices the response is not significant. This is due to the information “contained” in the unemployment rate, the 3 factors mentioned above that react differently depending on the state of the economy, the business cycle phase. A study on contagion carried out in 2013 by Beirne J. and Fratzscher examines this phenomenon over the period 1999-2011, covering a large number of countries, namely 31, distinguishing three types of contagion: a contagion related to quantitative and qualitative information contributing to the well-being of an economy - contagion due to a high sensitivity of financial markets, regional or spill-over contagion and herd contagion (considered pure contagion) - an effect generated by an exaggeration, a temporarily distorted reaction of financial markets, involving panic among investors; this makes the herd contagion extremely difficult to detect and measure. The study conducted by the European Central Bank analysts, Beirne J. and Fratzscher M., showed that the level of sovereign risk and its growth during the crisis is mainly explained by quantitative and qualitative information contributing to the welfare of the economy, while regional contagion does not explain the sovereign risk as strongly. Market volatility will continue to be discussed and studied in the desire to better understand the factors that generate it, how their effects can be foreseen, what are the investors’ behaviour in the moments of instability and how markets can be rebalanced. What follows in the remaining sections of the analysis is a presentation of the methodology used to derive the volatilities for the considered markets and to calculate the spill-over index, continuing with a description of the results and then summing up the conclusions.

2. Methodology

2.1 Estimating Market Volatility through GARCH Models

To determine which was the most sensitive Romanian financial market and how it responded to the emergence of financial shocks, the following markets were compared: the capital market – represented here by the bond market (not: PTS) and the stock market (not: PC), the monetary market (not: PM) and the foreign exchange market (not: PV) for the period August 2007 - May 2018, considering that as of August 2007, volatility in many markets had started to grow. A modeling of volatilities on these markets was pursued. In order to be considered reasonable models and the estimation to provide clear information, the number of daily observations entered in the model should be over 1000, this condition being met in this analysis with even more than 2500 daily observations. For the sake of consistency, the same period (August 2007 May 2018) was chosen for all four significant variables of the selected markets (Bucharest Exchange Trading BET index, Romanian Interbank Offer Rate ROBOR 3M, the yield on government securities 10y, and the EUR / RON exchange rate), starting with several observations and eliminating in the event that there were no transactions on that day on at least one of the For the stock market and the foreign exchange market, the values were converted into returns by applying the formula:![]() , while for the other two markets the difference xt+1 − xt was applied. By analyzing the correlogram for

, while for the other two markets the difference xt+1 − xt was applied. By analyzing the correlogram for

each of the considered variables, there was autocorrelation at lag 1, so by applying the ARCH test for one lag, we can reject H0 (there is no autoregression, we have homoskedasticity) with a probability of 0%, and we accept H1 (there is autoregression), having heteroskedasticity. Thus, GARCH (q, p) models are chosen to estimate the volatility of the studied markets. In practice, GARCH is preferred over ARCH which needs several lags (according to Gujarati (2003), GARCH(q,p) is equivalent to ARCH(q+p)). The GARCH model was subsequently extended to relax some assumptions regarding the parameters of the variation equation, or to incorporate the asymmetry of the impact of the yield on the financial assets, or to break the volatility into trend and short-term volatility. This is how asymmetric ARCH models, which allow analysis of asymmetric response to shocks appeared, out of which the most commonly used are the Threshold ARCH (TARCH) and GARCH Exponential (EGARCH) models. The generalized equation of the variance in a GARCH(p, q) model has the following form:

, where:

?0 − ?ℎ? ???????? ?? ?ℎ? ??????????? ???????? ????????

? − ?ℎ? ???? ?????????, ?ℎ??? ?ℎ? ????? ???ℎ ?ℎ??ℎ ?ℎ? ?????????? ?????? ?? ?ℎ???? ?? ?ℎ? ??????;

?2?−? − ?ℎ????, ???????? ??????????? ???ℎ ??????? ?? ?ℎ? ?????????? ???????? ???ℎ? ???????? ??????;

? − ?ℎ? ????? ?????????, ?ℎ??? ?ℎ? ?????????? ???????????;

?2t-j − ?????? ????????.

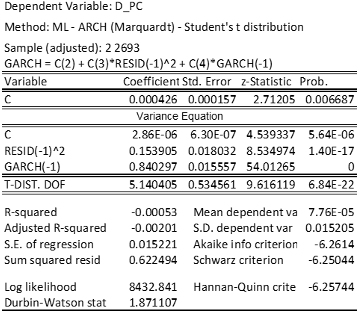

In the case of the stock market, the model for which all the coefficients were statistically significant, the log likelihood was maximal, and the AIC was the smallest is a GARCH(1,1) model for which a Student's t-distribution was considered for the errors. A decrease in log likelihood leads to an increase in the AIC information criterion and thus deteriorates the model's ability to be used in forecasting. Another criterion that a GARCH(q, p) model has to fulfill is that the sum of the ARCH and GARCH coefficients has to be in the range (0,1), which means that the unconditional variance of the error term is constant, and the process is not an explosive one. For modeling the volatility for the ForEx market an EGARCH(1,1,2) model was used.

The equation of the variance in an EGARCH model, for one lag, would be:

And for the particular case of this study

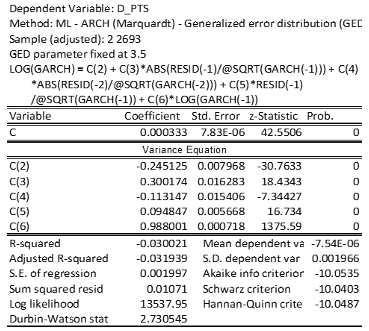

For the bonds market, according to the correlogram, there was autocorrelation at the first 3 lags and giving the ARCH test there was also heteroskedasticity. To estimate the volatility an EGARCH(2,1,1) model was chosen. Generalized error distribution (with fixed shape parameter 3.5) was chosen to correct the variance equation, when errors are not normally distributed. The resulting equation is the following:

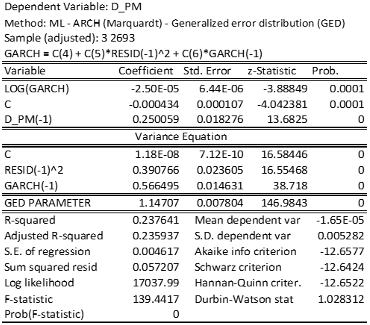

In addition to the previous models, in the case of the monetary market, in the mean equation the ROBOR 3M volatility (measured by log(variance)) was also introduced, its coefficient showing the effect of high-risk perception:

D_PMt = (1) ∙ log(?2) + ?(2) + ?(3) ∙ ?_???−1

log ?2 = ?(4) + ?(5) ∙ ??−12 + ?(6) ∙ ?2 ?−1

Using this model, certain conditions arise which in this case are fulfilled, namely: coefficients c(5) and c(6) must be positive and their sum should not exceed 1.

2.2 Computing the Spillover Index

The spillover index was calculated using an autoregressive vector with ten-step ahead forecast according to the methodology presented by Diebold and Yilmaz (2008) in their paper "Measuring financial asset return and volatility spillovers, with application to global equity markets". The measurement of spillover consists of estimating VAR models, concentrating on the decomposition of the forecast error variance, ultimately determining what percentage of the forecast error variance for one market is due to shocks both from that market and from other markets. In general, the formula they proposed for a pth order N-variable VAR with H step ahead forecasts is:

where: ?2h,ijis showing how much a shock to one variable contributes to the forecast error variance of another variable and ?????(?ℎ?′ ) expresses the total forecast error variation

3. Results

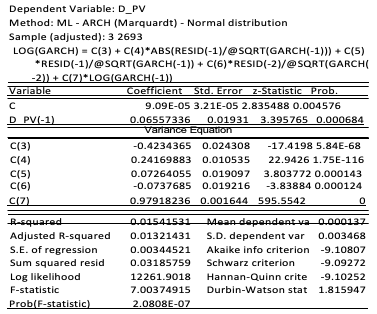

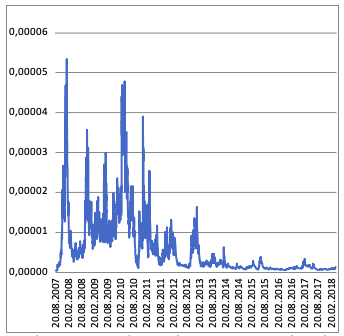

The foreign exchange market was the first to be affected by the global liquidity shortage and as a result of the ECB's injection of EUR 335 billion on the market (2008) it was expected that, with more money (euros) in the economy, the currency would depreciate.

Figure 1: Conditional Variance EUR/RON

Table following on the next page

Table 1: EGARCH(1,1,2) – ForEx market volatility (author’s computations in Eviews)

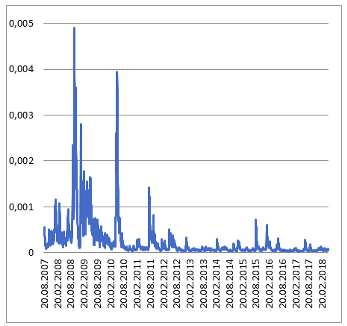

In the variance equation all the coefficients are statistically significant (as seen above), c(7) representing the coefficient of the exchange rate volatility and being positive means that when the volatility increases, the EUR / RON exchange rate will also increase, i.e. the RON is depreciating. According to the chart, the period with high volatility was January 2008 - November 2008 → period in which the euro’s value grew, possibly due to the ECB's increase in crediting and deposit interest rates, but also the increase of the minimum required reserve ratio by 0.25pp(the higher the MRR rate, the lower the liquidities and the borrowing between banks becomes more expensive). The interest rate rise and the appreciation of the euro led to an increase in the rates on euro loans, as the interest rate on euro loans in Romania is calculated based on the EURIBOR. The next impacted market was the bond market, having the peak in November 2008, the only year since 2000 when rating agencies anticipated a negative outlook for Romania and lowered its rating. Apart from the years 2008 - 2010, when the effect of the financial crisis and the sovereign debt can be clearly noticed, the attention is also drawn to the period 2011 - 2012, almost one year with higher volatility. This is precisely the time when Romania obtained a higher amount than expected from the 10-year bond sale on the US market (as opposed to the European market, still marked by financial instability) due to a bond issue program started in the month of June 2011. In January, Romania sold a record number of RON- denominated bonds at low interest rates in order to protect itself against a possible worsening of the sovereign debt crisis, being the largest amount attracted by the Government since April 2005. Romania knew to sell bonds early, at a time when risk appetite had stabilized. Between March and April 2010, Greece's major problems start to appear (high deficits, public debt levels of around 120% of GDP, high unemployment rate), and tough austerity measures were needed, which led to frequent strikes. Standard & Poor's drops the rating for Greece, with bonds reaching junk bond status. The ratings in Portugal and Spain also drop 1-2 positions.

Chart following on the next page

Figure 2: Conditional Variance 10y bond

Table 2: EGARCH(2,1,1) bond market volatility (author’s computations in Eviews)

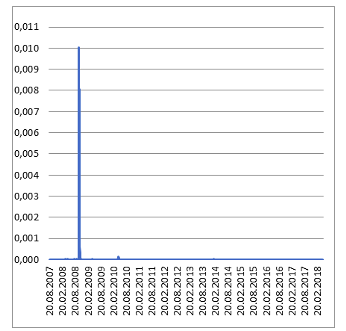

As far as the stock market is concerned, it is interesting that at the end of 2007 when the markets started to become unstable, the BET index registered its maximum (10,416.98), and by 2009 it collapsed to the value of 1,887.14. The Romanian stock market remains a frontier market, yet it does not reach the emerging market status. According to the FTSE Russell, we still do not have a well-developed stock market (due to the aggressive government intervention as a major or primary shareholder) and we do not meet the liquidity conditions. In order to move to an emerging market that would bring many more investors to Romania, there should be several significant privatizations and IPOs at the Bucharest Stock Exchange (e.g. Hidroelectrica), as well as a decrease of state holdings in companies such as OMV Petrom or Romgaz.

Chart following on the next page

Figure 3: Conditional Variance BET index

Figure 3: Conditional Variance BET index

Table 3: GARCH(1,1) stock market volatility (author’s computations in Eviews)

The fact that the volatility of the index is significant is also shown in Chart 3, which illustrates high volatility during the period 2008 - 2010. Even if the minimum value was reached in February 2009, the financial crisis has made its presence felt on the Romanian stock market since September 2008, shortly after the announcement of Lehman Brothers bankruptcy. In the financial markets it was noticed that the agents perceive volatility differently, depending on the direction of the change in the value of the respective financial asset. For example, for stocks, a downward movement of the market is followed by a higher volatility as compared to an upward movement of the same amplitude (leverage effect). The monetary market responded to the financial crisis through an explosive root, the ROBOR 3M index increasing its value from around 15% to 50% within a few days, and also having a rapid recovery. Starting with 2015, the interest rate was maintained between 0.5% and 1.5% until the end of 2017, followed by a period of sudden growth.

Chart following on the next page

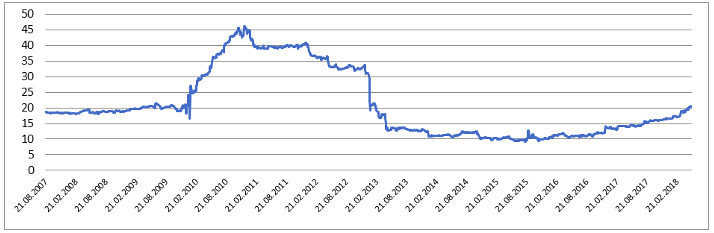

Figure 4: Conditional Variance ROBOR 3M

Table 4: GARCH(1,1) ARCH-M monetary market volatility (author’s computations in Eviews)

What is interesting to note is that while the ROBOR's maximum value in the analysed period was on October 20th, 2008, the market volatility increased abruptly from even before that, from October 17th. Unfortunately, this explosive root is what makes the variable more difficult to model, that value being an outlier. Considering the descriptive statistics and the estimated volatilities, we could say that the foreign exchange market and the capital market were the worst affected, the recovery was slow, which is understandable, considering that until the calming of the markets, investors preferred to limit their investments or to focus on safer assets: such as gold, oil. Only after 2012 investors have begun to regain their confidence in the Romanian markets after Standard and Poor's, as well as other rating agencies. announced steady prospects for Romania with a BB + rating. From the above analysis, it can be said, comparatively, that the most volatile market is the stock market, followed by currency and then monetary and bond markets. Having these results, I proposed a dashboard of the financial markets’ volatilities in order to easily capture their evolution over the period under review:

Legend:

volatility - High volatility

![]()

Figure 5: Volatility dashboard – financial and sovereign debt crisis period (author’s computations in Excel)

The period with significant volatility is represented by the years 2008-2009, with the peak in October 2008. The year 2010 is also marked by high volatility in the first 8 months, predominant in the bond market, due to the intensification of the sovereign debt crisis and a possible contagion effect coming from the more severe affected countries in Europe. In 2011 the volatility in the foreign exchange and bond markets continued, with all markets stabilizing by the end of 2014.

Figure 6: Volatility dashboard – post crisis period (author’s computations in Excel)

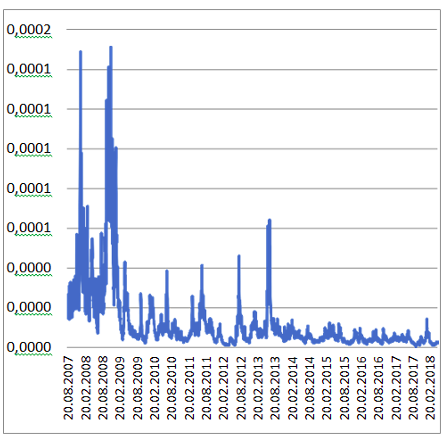

It is noteworthy that the volatility in the ForEx(PV) and capital markets(PC) is felt at moments of minimum wage increase (January and June). In June 2016, we can consider another possible cause of volatility for the capital market, namely the announcement of the referendum outcome by which British citizens voted for Britain's exit from the EU. January 18th - March 5th, 2017 was a period dominated by protests against political corruption as a result of the Romanian government's intention to amend the Criminal Code on amnesty. Volatility on the foreign exchange market is due to the depreciation of the RON due to the deepening of the trade deficit. In terms of the monetary market(PM), ROBOR 3M has a sudden growth in October 2017, then stabilizes at that new level, but from April-May 2018 the increase continues. This was generated by the wages increase for the public sector, and so more money in the economy contributed to increased consumption and thus inflation. Consequently, the demand for liquidity is higher and interbank lending becomes more expensive. Instead, if banks would raise deposit rates to attract liquidity from the market and not from interbank loans, it would limit this trend of ROBOR growth. Through this volatility panel, we can see once again that the most volatile markets are currency and stock markets. The topic of contagion on the financial markets in Romania is further on considered, in order to determine the most sensitive markets and to calculate a spillover index. This index is a way to measure to what extent the spillover effect is due to internal shocks and how much it is due to shocks from other markets. The index reflects the magnitude and persistence of the shocks, and the following chart shows the market's reaction to the sovereign debt crisis, which began in 2010, intensified in 2011 with the turmoil on the European markets, which led to a much wider fluctuation of the spillover index. Being such a major economic event, it explains why the shock has spread (“spilled”) and impacted all the markets considered. What is notable is that the current value of the index reached the level it had in 2007/2008, in the economic boom period, before the global crisis started.

Figure 7: Spillover index (author’s computations in Excel, based on results from Eviews)

4. Conclusion

With regards to the financial markets considered in this study (stock market, bond market, monetary market, foreign exchange market), the article shows which are the most sensitive to the impact of the financial shock (being the ForEx and the stock market), over the period 2007 2018. The evolution over time is analyzed, their volatility is estimated using GARCH models, and all the results obtained are correlated with events, news and market information from those periods of instability. This is useful in order to better understand how these were translated into the behavior of investors and how their decisions were influenced. Because of uncertainty on some markets, investors are turning their resources to other markets, where they have more confidence or they consider safer for their investments, causing imbalances. The behavior of investors, as they react to the emergence of a shock, is decisive and extremely important in anticipating the effects that an unexpected event can produce. For an easier way of examining the markets’ volatility, the values were included into a dashboard. Apart from the financial crisis, high volatility on the ForEx market could also be explained by a rise in crediting and deposit interest rates and by the increase of the minimum required reserve rate. The bond issue program thanks to which Romania managed to attract a large amount of money could have generated volatility on the bond market. Nevertheless, it is also possible that countries such as Greece, Portugal and Spain, which were facing severe austerity measures caused by the deepening of the crisis, to have had also an impact on the instability on the Romanian market. Furthermore, there have been other events that have translated into a higher degree of volatility: raising the minimum wage, the Brexit, protests against corruption, the raise of salaries for the public workers which has created instability in the monetary market. A spillover index is also computed, and it only confirms the significant vulnerability period (2010-2012) that affected all the markets, period during which the phenomenon of contagion could have occurred.

References

- Beirne, J., Fratzscher, M. (2013). The Pricing of Sovereign Risk and Contagion during the European Sovereign Debt Crisis. Journal of International Money and Finance 34, 60–82 Crossref

- Boyd, J. H., Hu, J., Jagannathan, R. (2005). The Stock Market's Reaction to Unemployment News: Why Bad News Is Usually Good for Stocks. Journal of Finance, American Finance Association, vol. 60(2), pages 649-672, 04. Retrieved from Crossref

- Codirlaşu, A. CFA. (2007). Econometrie aplicata utilizand EViews 5.1- Note de curs. Programul de Master Specializat Managementul Sistemelor Bancare. Retrieved from http://www.dofin.ase.ro/acodirlasu/lect/econmsbank/econometriemsbank2007.pdf

- Diebold, F., Yilmaz, K. (2008). Measuring financial asset return and volatility spillovers, with application to global equity markets. Research Department of Federal Reserve Bank of Philadelphia, Working Paper no. 08-16

- Diebold, F., Yilmaz, K. (2010). Better to Give than to Receive: Predictive Directional Measurement of Volatility Spillovers. Forthcoming, International Journal of Forecasting. Crossref

- Eurostat database: http://ec.europa.eu/eurostat/data/database

- Gherguţ I., Oancea B., Capatana C., (2013). Modelarea volatilitaţii indicelui BET-FI, Revista de Statistica, Retrieved

- Ionescu, A. (2017). Creşte costul finanţării deficitului bugetar: Titlurile de stat ale României, în topul celor mai mari creşteri de Retrieved from http://cursdeguvernare.ro/creste-costul-finantarii-deficitului-bugetar-titlurile-de-stat-ale- romaniei-in-topul-celor-mai-mari-cresteri-de-randament.html

- Ionescu, A. (2017). România a ratat promovarea la statutul de piață emergent. Retrieved from

- http://cursdeguvernare.ro/romania-a-ratat-promovarea-la-statutul-de-piata-emergenta.html

- NBR Financial Stability Reports (2015), (2016), (2017). Retrieved from https://www.bnr.ro/PublicationDocuments.aspx?icid=6877

- NBR database: http://www.bnro.ro/Baza-de-date-interactiva-604.aspx

- România, pe primul loc în rândul Piețelor de Frontieră, cu randamente care depășesc 40% pe bursă. (25.07.2017). AGERPRES. Retrieved from https://www1.agerpres.ro/economie/2017/07/25/romania-pe-primul-loc-in-randul-pietelor- de-frontiera-cu-randamente-care-depasesc-40-pe-bursa-10-31-03

- Sif-urile si Fondul Proprietatea / S.T.E.A.M. - planul de acţiuni pentru obţinerea statutului de piaţă emergentă: BVB a eşuat în obţinerea statutului de piaţă emergentă, şi de la MCSI, şi de la FTSE Russell. (31.01.2018). Ziarul Bursa. Retrieved from http://www.bursa.ro/sif- urile-si-fondul-proprietatea-steam-planul-de-actiuni-pentru-obtinerea-statutului-de-piata- eme...&s=print&sr=articol&id_articol=339736.html

- Sonders, L.A. (2019). Panic Is Not a Strategy—Nor Is Greed. Retrieved from: https://www.schwab.com/resource-center/insights/content/panic-is-not-a-strategy-nor-is- greed

- Stancu, S. (2012). Efectele crizei datoriilor suverane asupra echilibrului la nivel macroeconomic, Revista Studii şi cercetari de calcul economic şi cibernetica economica a facultaţii de Cibernetica, Statistica şi Informatica Economica din cadrul ASE Bucureşti.

- Steiner, S. (2012). Timeline of European debt crisis. Retrieved from https://www.bankrate.com/banking/timeline-of-european-debt-crisis/

- Stobierski, T. (2018). What Causes Volatility in the Markets? Retrieved from https://www.northwesternmutual.com/life-and-money/what-causes-volatility-in-the- markets/

- Timeline: The unfolding eurozone crisis. (2012). Retrieved from http://www.bbc.com/news/business-13856580

{kind=link}