Journal of International Business Research and Marketing

Volume 3, Issue 2, January 2018, Pages 16-18

Cross-Generational Investment Behavior and the Impact on Personal Finance

DOI: 10.18775/jibrm.1849-8558.2015.32.3002

URL: http://dx.doi.org/10.18775/jibrm.1849-8558.2015.32.3002

1 Alexander Zureck, 2 Julius Reiter, 3 Martin Svoboda

1 FOM University of Applied Sciences, Germany, and Department of Finance, Masaryk University, Czech Republic

2 FOM University of Applied Sciences, Germany

3 Department of Finance at Faculty of Economics and Administration, Masaryk University, Czech Republic

Abstract: The purpose of this paper is to investigate socio-economic development condition and convergence evaluation in the EU-28 states in the context of the EU policy goals. The aim of this research is to estimate socioeconomic disparities and convergence problems in the European states by applying real valuations of well-being situations and economic development challenges in the EU member states. The research methodology is based on the European Commission legitimate documents application and socio-economic strategies, on the convergence theory and convergence scenario calculations along with socioeconomic forecasts analysis in the EU states. This research presents information about different socioeconomic indicators, indexes, and scheme of information`s flows for convergence level estimation. This study contains objectives and general outlines of period 2014-2020 in the framework of Europe as a whole, as well its impact on the EU member states economies and living conditions. Changes in the main socioeconomic concepts impact on EU convergence policy and rapidity of convergence depends on the initial discrepancy of the development level in the EU states. The efficiency of European convergence policy can also be improved by significant economic growth and by a clever choice of the country-specific social activities. This research investigates above information for social situations estimations in EU states as well as GDP growth, unemployment, population's income level and different welfare indicators. The main results reflect the overall economic situation valuation in the EU countries and present European convergence policy's impact on social development in the European states. The conclusions contain socio-economic situations appreciation in the context of European strategy goals and social inequality problems clarification in the EU states.

Cross-Generational

Keywords: Personal finance, Investment behavior, Young people, Retirement

Cross-Generational Investment Behavior and the Impact on Personal Finance

1. Introduction

In Germany, living people are stronger forced to deal with their own personal finances due to changes by the government years ago. In the past, the state pension was enough to have an acceptable life in retirement age and an income from the personal finances was a bonus. In recent times, the German government shifts the responsibility for retirement more and more onto the individuals (Svoboda & Zureck, 2015). Cross-Generational

Cross-Generational

Parallel to other countries, like the United States, consumers are more and more confronted with financial decisions. Most financial decisions have to be made in early life. On the one hand, younger people have to finance their educations and on the other hand, young people have to make financial decision due to their retirements (Lusardi, Mitchell, & Curto, 2010). Internationally, the level of debt is high in younger society. This has effects on major labor decisions and on retirement (Lusardi et al., 2010). At the end, the chance to become insolvent is higher if the level of debt is high (Roberts & Jones, 2001). Repaying the outstanding debts leads to the problem that people are not able to save money in special financial products for retirement like employer-provided pensions (Lusardi et al., 2010). Cross-Generational

Cross-Generational

There are several studies that illustrate that young people have a lack due to financial knowledge. The situation in Germany is comparable to the situation in the United States (NCEE, 2005; Reiter, Frère, Zureck, & Bensch, 2015). Low financial literacy has an impact on the level of debt. People with low financial literacy tend to have higher debts than others (Lusardi & Tufano, 2015). Furthermore, they do not invest in the stock market (van Rooij, Lusardi, & Alessie, 2011), pay higher fees for unsuitable financial products (Hastings & Tejeda-Ashton, 2008), and they do not have a plan for retirement (Lusardi & Mitchell, 2011, 2007). Cross-Generational

Cross-Generational

Whether the financial literacy is high or low depends on several aspects. One important factor is the parental home. Parents pass their financial literacy to their children. If the parents invest in the stock market, the chance is higher that their children invest in the stock market, too (Chiteji & Stafford, 1999). In addition, education in financial issues has influences on financial literacy. For example, the Czech Republic has a national strategy on financial literacy. The situation in Germany is different. Each federal state is responsible for the topics in school and university, also for financial literacy (Zureck & Svoboda, 2015). People with low financial literacy are not able to handle their own financial decisions due to retirement planning. Those people are not able to see the advantages and disadvantages of the existing financial products and a critical comparison of the alternatives is not possible (Lusardi et al., 2010). Cross-Generational

Cross-Generational

The aim of this paper is to analyze the investment behavior of young people in contrast to older ones. It should give an outlook to consequences of the current investment behavior on to retirement and social wealth of the young generation. Cross-Generational

2. Methodology and Data

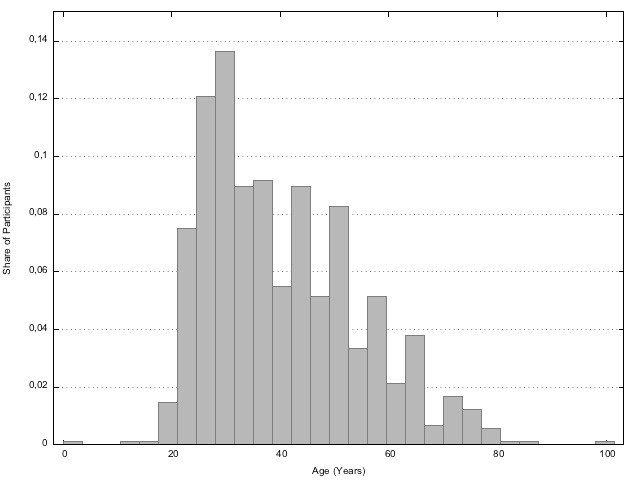

Figure 1: Participants by Age

Source: Own calculation

In total, participants’ monthly savings ratio is between 400 EUR and 500 EUR. The participants save monthly on average between 100 EUR and 200 EUR for retirement. Figure 2 shows that most people save money for retirement and the total amount increases by age.

Figure 2: Monthly Savings Ratio for Retirement

Source: Own calculation

A logistic regression permitted us to assess which factors are linked to investment behavior. We examine different specifications. These specifications allow us to identify more influencing variables. We consider the case where the response SFIi is binary. It is defined as follows:

![]()

Formula 1: Definition of Secure Financial Investment

In this paper, secure financial investments are called money, fixed deposit, savings book, or building loan contract. The regression model is as follows: Cross-Generational

SFI* = a + b(age) + c(male) + d(partnership),

Formula 2: Regression model

where SFI* is the dependent variable: an investor's propensity to invest in a secure financial investment. Age, male, and partnerships are observable independent variables. A is constant. B, c, and d are parameters that have to be estimated. Cross-Generational

Cross-Generational

We tried to take into consideration some other variables. The professional qualification, university degree, children, and the type of employment have not improved the model. The explanatory power of other models with more independent variables is weaker. Cross-Generational

3. Results and Discussion

The following part includes the results from the beforehand described logit regression. Figure 3 below represents the logit regression model where the dependent variable is binary variable:

Figure 3: Results of the logit regression model

Source: Own calculation

Figure 3 shows that the investment behavior depends on investor’s age, sex, and marital status. Other specifications of the model with more including variables have no more results. For example, we took into consideration the subjective financial knowledge. It has no influence on the investment behavior concentrating on secure financial investments. This is the reason why we are not able to confirm the importance of high financial literacy for the field of secure financial investments.

Cross-Generational

The coefficient of the variable age demonstrates that younger people prefer secure financial investments. Absolutely, the effect is weak but the tendency is clear. Therefore, we are able to add an important aspect to the general statement by Lusardi, Mitchell, and Curto: "[…] financial mistakes made early in life can be costly" (Lusardi et al., 2010). Secure financial investments are normally low-return investments. German young people are risk-averse and therefore they have a financial disadvantage for a long period because of missed returns from e.g. stocks or bonds.

Cross-Generational

Moreover, the results illustrate that especially women prefer secure financial investments. With a coefficient of 1.24899, the effect is strong. Additionally, the coefficient for the variable partnership emphasizes the effect. Because people living in a partnership tend to invest in secure financial investments. A question for future research can be how sex’s investment behavior is influenced by the partner. So, it is possible to improve the understanding of household's investment behavior in addition to past results for the fact that financial literacy is passed from the parents to their children (Chiteji & Stafford, 1999). Cross-Generational

Cross-Generational

Young people prefer to invest in secure financial investments like call money, fixed deposit, savings book, or building loan contract. Parallel, the level of debt is higher than in older generations (Lusardi et al., 2010). Younger people have to accept lower returns because of their investment behavior as well as the low-interest level. Furthermore, they have to repay their debts. Both aspects lead to the situation that there is a latent risk that young people haven’t got enough money in retirement age. The state has to deal with this situation in its own interest. The state has to take care that young people learn to manage their own financial situation. Otherwise, the state has to offer social protection in the event of retirement. That is the reason why the state has to improve financial literacy. High financial literacy leads to better financial decisions and a better social wealth in general. Cross-Generational

4. Conclusion and Outlook

Secure financial investments are popular for young people. That has the influence on the generated returns of young people. The risk-averse investment behavior leads to the problem that returns do not improve the wealth situation of young people. If the young investors will not change their investment behavior, there is the latent risk that they do not have enough in retirement age. This fact is more actual than ever because of the low-interest phase. The level of debt in the younger generation strengthens the situation. Cross-Generational

Cross-Generational

It is the interest of the state that everybody has social protection in the event of retirement. Therefore, the state has to improve financial education or the pension system. An improved financial literacy leads to the advantage that people concentrate more on risky investments like stocks etc. as an investment alternative. Without these investment alternatives, people are not able to get an acceptable return that guarantees social protection in retirement age.

Cross-Generational

At the end, the paper shows that younger people like investing in secure financial investments. Additionally, women and people living in a partnership prefer this kind of financial products. The trend to invest in low-interest financial products can have negative impacts on retirement plans. There is the risk that these people will not have enough money in retirement age.

References

- Chiteji, N. S., & Stafford, F. P. (1999). Portfolio Choices of Parents and Their Children as Young Adults: Asset Accumulation by African-American Families. American Economic Review, 89(2), 377–380. Crossref

- Hastings, J., & Tejeda-Ashton, L. (2008). Financial Literacy, Information, and Demand Elasticity: Survey and Experimental Evidence from Mexico. Cambridge, MA. Crossref

- Lusardi, A., & Mitchell, O. (2011). Financial Literacy and Planning: Implications for Retirement Wellbeing. In A. Lusardi & O. Mitchell (Eds.), Financial Literacy: Implications for Retirement Security and the Financial Marketplace. Cambridge, MA: Oxford University Press. Crossref

- Lusardi, A., & Mitchell, O. S. (2007). Baby Boomer retirement security: The roles of planning, financial literacy, and housing wealth. Journal of Monetary Economics, 54(1), 205–224. Crossref

- Lusardi, A., & Tufano, P. (2015). Debt literacy, financial experiences, and overindebtedness. Journal of Pension Economics and Finance, 14(4), 332–368. Crossref

- Lusardi, A., Mitchell, O. S., & Curto, V. (2010). Financial Literacy among the Young. Journal of Consumer Affairs, 44(2), 358–380. Crossref

- (2005). What American Teens & Adults Know About Economics. The National Council on Economic Education.

- Reiter, J., Frère, E., Zureck, A., & Bensch, T. (2015). Finanzberatung: Eine empirische Analyse bei Young Professionals (4th ed.). Essen.

- Roberts, J. A., & Jones, E. (2001). Money Attitudes, Credit Card Use, and Compulsive Buying among American College Students. Journal of Consumer Affairs, 35(2), 213–240. Crossref

- Svoboda, M., & Zureck, A. (2015). Kritische Analyse der Financial Literacy im internationalen Vergleich. In E. Frère & S. Reuse (Eds.), Risk- und Invest management am Finanz- und Kapitalmarkt (Finance) (pp. 19–31). Essen: MA Akademie Verlags- und Druck-Gesellschaft.

- van Rooij, M., Lusardi, A., & Alessie, R. (2011). Financial literacy and stock market participation. Journal of Financial Economics, 101(2), 449–472. Crossref

- Zureck, A., & Svoboda, M. (2015). Financial Literacy: An International Comparison between Germany and the Czech Republic. In V. Kajurová & J. Krajíček (Eds.), European Financial Systems 2015. 12th International Scientific Conference (pp. 704–709). Brno: Masaryk University.

{kind=link}