International Journal of Management Science and Business Administration

Volume 6, Issue 3, March 2020, Pages 29-42

Financial Ratios as Predictors of Financial Distress: A Study on Some Select Deposit Money Banks in Nigeria (1991-2014)

DOI: 10.18775/ijmsba.1849-5664-5419.2014.63.1003

URL: http://dx.doi.org/10.18775/ijmsba.1849-5664-5419.2014.63.1003

1 Ojeabulu Uyi Michael, 2 Chigbu E. Ezeji, 3 Ozurumba A. Benedict,

4 Kanu Success Ikechi1 2 3 The Department of Management Technology (FMT), School of Management Technology, Federal University of Technology, Owerri, Imo state Nigeria

4 The Faculty of Social and Management Sciences, Eastern Palm University, Ogboko, Ideato South LGA, Imo State, Nigeria

Abstract: The purpose of this study is to evaluate the use of financial ratios as a predictor of financial distress in Deposit Money Banks (DMB) in Nigeria. Banks’ deficiency in the period between 1991 and 2011 and a subsequent loss of depositor’s funds first prompted our attention. The instability of the industry felt even today calls for further research to understand the underlying causes of such issues better. Three Nigerian Deposit Money Banks were financially analyzed using data set for the period between 1991 and 2014. The banks were classified as very strong, strong, and weak. For instance, GT Bank was classified as very strong, UBA as strong, and Polaris bank as weak. Data were collected from the banks’ annual financial reports. Other sources were included, such as CBN Annual Reports and NSE Fact Books. Logistic regression analysis was performed on the data set. The model correctly predicted 87.5% of periods in which the banks were expected to experience financial distress and 93.8% of periods in which the banks were supposed to be in good financial state. Out of the five ratios that were used in the study, three turned out to be significant in predicting banks’ financial distress. This research constructed a model of financial ratios to predict difficulty with great success. Thus, stakeholders are advised to go beyond assessing the present status of banks, i.e., their strengths and weaknesses, but to utilize financial ratios in the near future. The study recommends that bank management should focus more on generating more earnings with the assets at their disposal.

Keywords: Bank distress, Financial ratios, Logistic regression, Prediction model

1. Introduction

The banking sector is the vein of any modern economy. Banks’ ability to achieve targeted results relies upon adherence to rules and regulations, while a deviation may cause a breakdown. In the prior research, the causes of unhealthy deviation from set rules have been discussed to include inadequate supervision, weak management, and ineffective government policies. Ogunleye (2002) classified the causes of bank failure into institutional, economic and political factors as well as regulatory and supervisory inadequacies. Ebhodaghe (1995) attributed bank failure to financial deficiencies, economic downturn, negative policy environment and management problems.

The impact of deficiency in the banking sector usually has a further effect beyond the industry. In this spirit, predicting distress in the industry becomes imperative. Financial distress is a situation where an entity or a firm cannot meet its business goals or is having difficulty in fulfilling its financial obligations to creditors. It could be said that, while the banking failures of the pre-90s could be reduced to inadequate regulatory frameworks, such failures grew unabated even when regulations were set. This includes Banks and Other Financial Institutions Decree (BOFID) of 1991, prudential guidelines on asset classification, provision for loan losses (SAS 10), Failed Banks (Recovery of Debts), etc. These failures had underscored public confidence in the system and had resulted in massive withdrawal of funds from failed banks to the healthier ones.

In 2007, the banking sector consolidation and the capitalization of bank stocks set the stage for a financial asset bubble, particularly in bank stocks. According to Sanusi Lamido Sanusi (2012), the massive surge of capital availability occurred in the period when corporate governance standards in the banking sector were fragile. It is pertinent to mention here that, even when these signs of distress or failures were imminent, the Central Bank of Nigeria (CBN) failed to communicate the problem to fiscal authorities and the market in general and this also aided or exacerbated the crisis. To forestall a re-occurrence of the messy pasts, it became necessary to develop safety catch nets that could help banks foresee when they are heading for the rocks. This is where the use of predictive ratios and models comes in. Identifying a corporate failure or distress as early as possible is a matter of considerable interest to all the stakeholders as the banking sector requires constant monitoring, surveillance and appraisal to stay on course. The broad objective of this study is to ascertain the class or set of financial Ratios or models that may help to detect unforeseen bank distress as early as possible.

Therefore, we intend to find answers to the following research questions:

- Is Working Capital to Total Assets ratio a better and more significant predictor of bank distress?

- Is Retained Earnings to Total Assets ratio a better and more significant predictor of bank distress?

- Is EBIT to Total Assets ratio a better and more significant predictor of bank distress?

- Is Value of Equity to Book Debt ratio a better and more significant predictor of bank distress?

- Is Gross Earning to Total Assets ratio a better and more significant predictor of bank distress?

- To what extent can the aforementioned financial ratios be used to classify GT Bank, UBA, and Polaris banks as very strong, strong and weak banks, respectively?

To answer this, we hypothesized the following:

- Working Capital to Total Assets ratio is not a better and more significant predictor of distress.

- Retained Earnings to Total Assets ratio is not a better and more significant predictor of distress.

- EBIT to Total Assets ratio is not a better and more significant predictor of distress.

- Value of Equity to Book Debt ratio is not a better and more significant predictor of distress.

- Gross Earnings to Total Assets ratio is not a better and more significant predictor of distress.

- The five ratios (Working Capital to Total Assets, Earnings to Total Assets, EBIT to Total Assets, Value of Equity to Book Debt and Gross Earnings to Total Assets) cannot be used in classifying the three banks (GT Bank, UBA and Polaris) into weak, strong and very strong categories.

Because the Nigerian economy has suffered several financial distresses, and there is a lack of available resources to predict the future state of the financial sector, we find this analysis will provide a greater insight into the mechanisms leading to demise. Many depositors and investors alike lost their life savings and funds. This brought about an untold hardship to the banking public. People with different backgrounds have commented on this seemingly intractable and recurring problem as it seems to have touched on the very fabric of the nation’s economic life.

Thus, this study is set to investigate the matter by establishing the causes, consequences and providing recommendations as to how we can prevent distress in the banking industry of Nigeria via predictive financial ratios and models. This study will be of immense benefit to bankers as the predictive models will give a clue to the health status of their business. Students of Business and organizational affairs will also benefit from this study as it will elicit further investigation on financial ratios and distress in other economic sectors. Investors and depositors will be able to make better and informed investment decisions based on the health of the organizations they want to invest in. Our results will also prop the regulatory authorities into action. This will help to forestall any financial crisis or loss of confidence in the financial system. Our recommendations will also be helpful and applicable to other sectors of the economy. A discussion of banking sector distress is a worldwide phenomenon; however, this study is restricted to only three (3) Nigerian banks, namely Guaranteed Trust Bank (GT Bank), United Bank for Africa(UBA) and Polaris Bank (Former Afribank /Skye Bank). The scope of this study is delineated from 1991 to2014.

2. Literature Review

2.1 Conceptual Framework

The role of accounting information in distinguishing between firms/ companies with financial distress and those without financial difficulty had been one of the controversial issues in the recent past. Studies by Altman (1968) and Blurn (1974), indicate that from using multivariate models and accounting information, it is possible to detect companies that are about to face financial distress. Financial distress and finally, bankruptcy can cause some considerable damages to shareholders, investors, creditors, managers, employers, suppliers of raw materials and other clients. It can be said that the detection of a company operating with financial difficulty is a subject that has been particularly amenable to analyses using financial ratios.

Banking Business and Distress

According to Benston (1986), a bank becomes insolvent when the present value of her net worth becomes zero. At this point, the current value of a bank’s total assets is equal to the present value of its deposit and non-deposit liabilities other than equity capital”.

At least economically, the bank no longer belongs to the shareholders, but to its creditors (including depositors and deposit insurance agencies, if any). When declared insolvent, the bank is considered to have failed, a phenomenon that results from financial distress. A bank fails when there is a regulatory induced cessation in its operations as an independent entity free of direct interrelation and oversight by a regulatory agency (Benston et al., 1986). Banking as a service industry fundamentally operates on trust and is sustained by attitude and managed by employing complex financial management skills and psychology of human relations. The more the customer trusts the service provider, the higher the perceived value of the relationship (Walter, Holzle and Ritler, 2002).

The quality of bank services is influenced indirectly by trust. Trust is considered to be the cornerstone of the banking industry, and perceptual factors will affect the customers’ choice of bank. Moreover, for the development process, the banking industry acts as a catalytic agent, which makes a healthy banking system ‘a must’ for a nation’s growth. Conversely, a near or total distress in the banking industry is harmful to the entire society.

Indicators used in foretelling banking distress range from declining output, an increase and then a decrease in inflation to a fall in the real effective exchange rate. The primary direct indicator of banking sector soundness and the likelihood of the distress is the level of bank capitalization, that is, the amount by which a bank’s assets exceed its liabilities. Bank distress is associated not only with bank failure but also with macro-economic consequences resulting from the reduced supply of loans and deposits. This decline amplifies the business cycle on turns and spread of panic-induced financial distress from banks spills to the entire economy.

Overview of Bank Distress in Nigeria

The problem of bank distress in the Nigerian banking sector has been ongoing since the 1930s. In between 1930 and 1958, over 21 failures were recorded. The bank failures during that era may have been caused by the domination of foreign banks in terms of the exclusive patronage by British firms (Soyibo and Adekanye, 1992). Other factors that led to the mass failure of the indigenous banks were low capital base, lack of managerial expertise and untrained personnel (CBN, 1997). The deregulation of the financial system started in 1986 as part of the Structural Adjustment Programme (SAP). The deregulation brought about strict changes in bank operations and regulatory environment, and the distress syndrome resurfaced again in Nigeria.

Following this, the policy-induced consolidation of the banking industry, starting from July 2004 and completed by 31st December 2005, also brought with it distress in the banking sector in Nigeria. It will be recalled that on 1st January 2006, 25 banks emerged from 75 of the 89 banking institutions that existed at the end of June 2004. The remaining fourteen (14) banks with negative net worth had their licenses revoked and were handed over to NDIC for liquidation.

The significant causes of banking sector distress in Nigeria could be attributed to the following factors:

- Insider Lending.

- Lending to High-Risk Borrowers

- Macro-Economic Instability and

- Non-adherence to liquidity Support and Prudential Regulation

Effects of Bank Distress

In the 1980s and early 1990s, several countries, including Nigeria, experienced severe banking crises. Such proliferation of large scale banking sector problems raised widespread concern, as banking crises disrupted the flow of credit to households and enterprises, reducing investment and consumption and possibly forcing viable firms into bankruptcy. Banking crises may also jeopardize the functioning of the payments system by undermining confidence in domestic savings and/or a large scale capital outflow. Finally, a systemic crisis may force sound banks to close. In most countries, policymakers have attempted to shore up the consequences of banking crises.

The Concept of Capital Adequacy in Banking

The efficient functioning of markets requires participants to have confidence in each other’s stability and ability to do business. Capitals' rules help foster this confidence because they need each member of the financial community to have, among other things, adequate capital. This capital should be sufficient to protect the financial organization’s depositors and counterparties from the risk of the institutions’ on and off-balance sheet risks.

Significance of Capital Adequacy in Nigerian Banks

According to Adewumi (1997), since the early ’70s, great concern was the issue of ensuring the adequate capital for banks. The industry has witnessed unprecedented competition in the last three decades. This has led bankers to engage in new and riskier ventures, resulting in supervisory authorities’ concern over capital adequacy. In Nigeria, the interest of regulatory authorities has been reflected in the continual increase in the capital requirement for banks entering the industry. Furthermore, as a result of inflation, the column of banking business reflected in the total assets/liabilities of banks has increased phenomenally in recent years as the asset will diminish in relation to liabilities if no addition is made to it. This trend raised concerns of regulatory authorities all over the world. It is also imperative to stress that the international business environment and sectors have become increasingly intertwined as a result of globalization. “Globalization of business is an innovative development in the business world, which lowers or removes international trade barriers and render all locations of the economic world relatively accessible, thereby turning the financial world into one giant global village (Nwezeaku, 2006). The impact of consolidation on the stability of banks in Nigeria can be seen from the perspective of Increased Capital Flow, Increased Lending Capacity and improved access and exposure to the Capital Market. The consolidation also ushered in an unprecedented era of new listings of new banking stocks.

Corporate Governance and Bank Performance in Nigeria

Corporate governance has, in recent years, assumed considerable significance as a veritable tool for ensuring corporate survival. Since business confidence usually suffers each time a corporate entity collapses, most of the business failures in the recent past were attributed to a failure in corporate governance practices.

Prudential Guidelines

The introduction of the prudential guidelines is meant to bring order and harmony in the reporting of loan provisioning and classified risk assets. The prudential guidelines issued by the CBN in 1990 aimed at proper loan asset classification and income recognition. Before the introduction of prudential guidelines, banks had their methods of classifying accounts, rating credit and categorizing accounts as performing accounts. The implications of their actions led to the declaration of a high level of profit that was not realized.

2.2 Theoretical Framework

Financial statements provide crucial information to various users who have an interest in diverse fields. All financial statements are primarily historical documents. They disclose what happened during a particular period. However, most users of financial statements are concerned about the future. The information provided in the financial statement is of immense significance in decision-making through analysis and interpretation. Financial statement analysis includes the use of Horizontal or Trend Analysis, Vertical Analysis and Ratio Analysis.

Trend Analysis

The comparison of two or more years’ business organization’ financial data is known as a trend analysis. Horizontal analysis facilitates the process by highlighting changes between years in both currency (e.g., Naira) and percentage form.

Vertical Analysis

Vertical analysis is the procedure of preparing and presenting common size statements. According to Pandy (2004), a common-size statement is the one that shows items appearing on it in percentage form as well as in monetary form. Each item is stated as a percentage of some total of which that item is a part.

Ratio Analysis

A ratio simply presents one number expressed in terms of another. A ratio is a statistical yardstick employing which relationship between two, or various figures can be compared or measured (Pandy, 2003). The term “accounting ratios” is used to describe a significant relationship between values shown on a balance sheet, in a profit and loss account, in a budgetary control system, or in any part of accounting in an organization. Accounting ratios thus show the relationship between accounting data.

As owners of businesses require information relating to returns, appraisals and other investment-related decisions, the need for more financial information became more prominent and desired overtime. (Nwezeaku, 2006).

2.3 Empirical Review

It is noteworthy to mention that one critical characteristics common to those early researchers which persisted till today is the level of the lack of agreement as to which ratios are the best predictors of failure. For example, Winakor and Smith (1935) verified the efficiency of ratios as predictors of firms’ financial fortunes or misfortunes in the early 30’s. The results of their study imply that the ratio of net-working capital to total assets was the most accurate and consistent indicator with its decline ten years before the occurrence of financial difficulty. By the middle of the last century, Roy Foulke, in his study “Practical Financial Statement Analysis, posited that the non-liquid ratios are better measures of long term solvency while the liquid assets ratios are short-term predictors. This constituted a departure from the Merwin’s finding in which two of the best three predictors are liquid ratios (Foulke, 1953)

In more recent studies, Adekanye (1993), attempted to isolate the factors used to distinguish vulnerable from resistant commercial banks in Nigeria. The study covering the period from 1984 to 1989 and adopting Multivariable Discriminate Analysis (MDA) and the logit regression techniques, confirmed managerial efficiency to be the overriding determinant of commercial bank performance in Nigeria.

Olaniyi (2007) also employed MDA in assessing bankruptcy/failure potential/status of Nigerian banks using First Bank Plc (being the bank with the most extensive banking experience and excellent track record of consistent good performance) and Trade Bank Plc. (a bank adjudged to be financially unhealthy). The study covered five years between 1998/1999 and 2003. To achieve the objectives of the study, he used data from discriminating variables which included working capital, retained earnings, earnings before interest and tax, equity as well as total assets and total book debts. These were obtained from the annual audited accounts and reports of the banks under assessment. He opined that the management of banks, employees of banks, shareholders as well as depositors deserve a warning tool capable of measuring failure potential of any bank before making an unguided decision of putting their deposits, investment fund or accepting an offer for employment to avoid the impact of the imminent collapse of such a bank.

Wurim Ben Pam(2013), investigated the potency of the Multiple Discriminant Analysis Model in ascertaining the state of health of Nigeria’s Deposit money banks Two ‘failed’ and two non-failed banks (as adjudged by Central Bank of Nigeria) constitute the sample of the study within a five year period (1999-2003). Contrary to regulatory agencies’ stand, Z Scores of the two non-failed banks were below 1.80, indicating ill-health. The study also confirms the ill health of a bank (whose license has since been revoked) while the Z Scores of the second bank-hitherto classified as ‘failed bank’ – is found to be above 3.00. that the conclusion was that the MDA model is still a potent tool in the prediction of the potential of failure. The paper recommends the unification of the MDA model with other models.

Onyeiwu and Aliemeke (2013) investigated the use of financial ratios to ascertain the state of health of Deposit Money Banks in the Nigerian financial services sector using the multivariate analysis. Twenty-three banks constitute the sample, of which eight have been indicted as weak, by the Central Bank of Nigeria within the year of investigation (CBN 2009).The study applied a Multivariate technique to Nigerian banks to ascertain its ability to discriminate between weak and healthy banks. The audited report for the year ending in 2009 formed the basis of the calculation. The study provides the regulatory authorities insight on how the Z score can be used to improve their supervisory oversight function Kowanda, Pasaribu and Firdausi (2014) did a study on financial prediction on public listed banks in Indonesian stock exchange. They opined that the financial distress of a company should ably be anticipated smartly by its management to rerun the business without having any loss due to business failure. Thus, we need a model that could provide an early signal to the company so that remedial efforts can be run immediately. They explored CAMEL’s ratio as an early classificatory and also to reexamine the capacity of CAMEL ratio as a predictor of banks distress. Using a logit binary to classified the probability of distress and non-distress, then multiple regression to determines the ability of financial ratios as a predictor of distress, obtained the following results: a) An exploration CAMEL ratios as an early classificatory, resulting in high classification capacity with a range of 78.7%-91.4%, Furthermore, when CAMEL ratio was used as a predictor, still resulted in a high of the capability to classify samples accurately by 82.4%.

Karugu, Achoki and Kiriri (2018), sought to investigate the efficacy of capital adequacy ratios as predictors of financial distress in Kenyan commercial banks. The population of the study was drawn from 43 commercial banks operating in Kenya over the period 2009-2015. Data were collected from annual reports of commercial banks and analyzed using stepwise logistic regression. Hypothesis testing was done at 0.05 significance levels. The study found that capital adequacy ratios were significant predictors of financial distress in commercial banks in Kenya. The study concluded that capital adequacy ratios were significant predictors of financial distress in commercial banks. Consequently, the study recommended that there be introduced a continuous industry-driven regulatory and reporting structure on capital adequacy for commercial banks.

2.4 Review of Existing Studies and a Consequent Research Gap

Citing of different ratios as the best predictors of failure by various researchers only calls for more empirical research into the predictive powers of financial ratios rather than to invalidate any theory, it must be noted that these scholars, all agreed that ratios measuring profitability, liquidity and solvency are ratios which have prediction powers that are not in doubt. The interplay of extraneous factors, such as macroeconomic variables has not been extensively captured. It is also worthy of note that the complexity of the business environment requires industry-specific studies to be conducted as prediction models may vary across industries just as in business models. Variations in business models across different economic climes are factors that have not generally been considered in the study of distress. That is a research gap that we intend to fill in this study.

3. Research Methodology

Ex-post facto research design was used in the study. The population studied comprised all banking institutions in Nigeria that operated between 1991 and 2014. Three banks were selected using a judgemental sampling technique. The adjudged and selected very strong bank was Guaranty Trust Bank Plc(GT Bank), the strong bank was United Bank For Africa (UBA) and the adjudged weak bank was Polaris(Former Skye/ Afribank).

The study relied on data from financial statements of the select banks, as well as macroeconomic reports published by the regulatory authorities, i.e., CBN and NDIC.

Data were collected via a combined application of content analysis and data mining. Data is considered valid and reliable as it was directly extracted from secondary sources using content analysis and data mining. Data analysis was done using inferential as well as descriptive statistics.

Logistic regression was used in the study as it allows one to say that the presence of a risk factor increases the odds of a given outcome by a specific element.

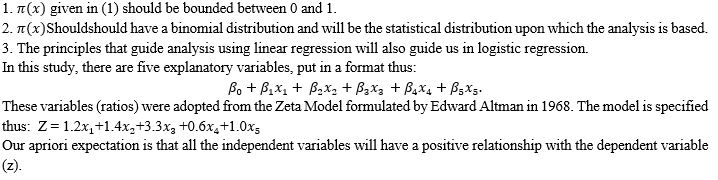

Model Specification

The specific form of the logistic regression model used was:

![]()

So we transform of (x). What is central to our study of logistic regression is the logit transformation. The transformation is defined in terms of as:

![]()

The importance of this transformation is that g(x) has many of the desirable properties of a linear regression model. The logit, g(x), is linear in its parameters, may be continuous and may range from ![]() depending on the range of x. The model should satisfy the following conditions:

depending on the range of x. The model should satisfy the following conditions:

4. Data Analysis and Interpretation

4.1 Data Analysis

Extracts from the financials of GT, UBA and Polaris banks were obtained and analyzed using a Logistic regression analysis. After running descriptive statistics, the data set for this study was divided into two, namely, healthy and weak deposit money banks. The healthy banks are GTB and UBA, while the weak is Polaris (Former Afribank)

Logistic Regression Analysis:

In logistic regression, the first task is to ascertain that the model is appropriate for the data; hence Hosmer and Lemeshow test was carried out. The p-value of Hosmer test is 0.445. The chi-square is 7.883, with the p-value exceeding 0.05, this implies that we accept the null hypothesis; that the observed and the predicted values of the response variable (y) do not differ statistically. Therefore, we agree that the model fits the data very well. Thus, the model is feasible for the study.

Table 1: Hosmer and Lemeshow Test

| Step | Chi-square | Df | Sig. |

| 1 | 7.883 | 8 | .445 |

Table 2: Contingency Table for Hosmer and Lemeshow Test

| Y = Weak | Y = Healthy | Total | ||||

| Observed | Expected | Observed | Expected | |||

| Step 1 | 1 | 7 | 6.976 | 0 | .024 | 7 |

| 2 | 7 | 6.673 | 0 | .327 | 7 | |

| 3 | 6 | 5.408 | 1 | 1.592 | 7 | |

| 4 | 2 | 3.388 | 5 | 3.612 | 7 | |

| 5 | 1 | .845 | 6 | 6.155 | 7 | |

| 6 | 0 | .548 | 7 | 6.452 | 7 | |

| 7 | 1 | .138 | 6 | 6.862 | 7 | |

| 8 | 0 | .018 | 7 | 6.982 | 7 | |

| 9 | 0 | .006 | 7 | 6.994 | 7 | |

| 10 | 0 | .001 | 9 | 8.999 | 9 | |

Source: SPSS 20.0 output

Selection of Predictor Variables

Next, a stepwise method is used to determine the important variables with respect to their contributions to explaining the response variable

Table 3: Iteration Historya,b,c,d

| Iteration | -2 Log likelihood | Coefficients | ||||||

| Constant | X1 | X2 | X3 | X4 | X5 | |||

| Step 1 | 1 | 65.488 | 1.843 | -2.516 | -1.260 | 5.893 | 4.220 | -9.879 |

| 2 | 56.513 | 2.000 | -3.268 | -5.942 | 11.858 | 9.399 | -13.435 | |

| 3 | 46.551 | 2.063 | -2.190 | -17.602 | 27.390 | 13.143 | -18.156 | |

| 4 | 38.068 | 2.312 | .315 | -33.161 | 53.215 | 17.360 | -26.714 | |

| 5 | 31.678 | 4.493 | 1.354 | -43.497 | 94.190 | 7.271 | -40.796 | |

| 6 | 29.990 | 5.701 | 1.883 | -55.016 | 126.940 | 4.115 | -49.639 | |

| 7 | 29.773 | 6.306 | 2.337 | -61.580 | 144.039 | 2.944 | -54.415 | |

| 8 | 29.768 | 6.414 | 2.467 | -62.924 | 147.287 | 2.792 | -55.351 | |

| 9 | 29.768 | 6.417 | 2.473 | -62.967 | 147.386 | 2.789 | -55.379 | |

| 10 | 29.768 | 6.417 | 2.473 | -62.967 | 147.386 | 2.789 | -55.379 | |

Table 4: Omnibus Tests of Model Coefficients

| Chi-square | Df | Sig. | ||

| Step 1 | Step | 61.890 | 5 | .000 |

| Block | 61.890 | 5 | .000 | |

| Model | 61.890 | 5 | .000 | |

Source: SPSS 20.0 output

The chi-square statistic is the change in the -2 log-likelihood from the previous step, block, or model.

The omnibus test measures how well the model performs if it is significant. Based on the above table, it is found that the p-value (0.000) is less than 0.05, implying that the model is fit and it performs credibly well.

Table 5: Model Summary

| Step | -2 Log likelihood | Cox & Snell R Square | Nagelkerke R Square |

| 1 | 29.768a | .577 | .801 |

| Source: SPSS 20.0 output | |||

Table 5 highlights the explained variation. In our estimation from the given model, it ranges from 57.7% to 80.1%, depending on whether we reference the Cox & Snell R2 or Nagelkerke R2 methods, respectively. Nagelkerke R2 is a modification of Cox and Snell R2, the latter of which cannot achieve a value of 1. For this reason, it is preferable to report the Nagelkerke R2 value. Hence we say that all the financial ratios considered contributed about 80.1% change to commercial banks financial health. This also connotes that the model is reliable to predict the financial distress of Nigerian commercial banks.

Using a cutoff value of 0.5, the model was able to correctly predict of 87.5% of the periods in which banks were expected to go into financial distress and 93.8% of periods in which banks were supposed to be in a good financial situation. The overall predictability accuracy of the logistic regression model was 91.7%, as shown in table 6 below.

Table 6: Classification Tablea

| Observed | Predicted | ||||

| Y | Percentage Correct | ||||

| Weak | Healthy | ||||

| Step 1 | Y | Weak | 21 | 3 | 87.5 |

| Healthy | 3 | 45 | 93.8 | ||

| Overall Percentage | 91.7 | ||||

| a. The cut value is .500 | |||||

Source: SPSS 20.0 output

Table 7: Variables in the Equation

Next is to ascertain, the variables or ratios that are significant in predicting the proportional of periods in which the banks were expected to be financially distress.

| B | S.E. | Wald | df | Sig. | Exp(B) | 95% C.I.for EXP(B) | |||

| Lower | Upper | ||||||||

| Step 1a | X1 | 2.473 | 4.352 | .323 | 1 | .570 | 11.856 | .002 | 60077.034 |

| X2 | -62.967 | 20.753 | 9.206 | 1 | .002 | .000 | .000 | .000 | |

| X3 | 147.386 | 46.996 | 9.835 | 1 | .002 | 1.021E+06 | 1.013E+02 | 1.029E+10 | |

| X4 | 2.789 | 11.394 | .060 | 1 | .807 | 16.272 | .000 | 8.124E+011 | |

| X5 | -55.379 | 17.940 | 9.529 | 1 | .002 | .000 | .000 | .000 | |

| C | 6.417 | 2.589 | 6.143 | 1 | .013 | 611.889 | |||

| a. Variable(s) entered on step 1: X1, X2, X3, X4, and X5. | |||||||||

Source: SPSS 20.0 output

Only three of the five ratios x2, x3 and x5initially entered into the logistic regression model were found to be significant in predicting the proportional time or periods in which the banks were expected to be financial distress. The estimated logit model is:

![]()

Going by the outcome of Table 7 above, we can now go ahead and test the afore-stated hypotheses, thus:

Test of hypothesis one: “Working Capital to Total Assets ratio is not a better and more significant predictor of distress.”

Comment/Interpretation: As shown in table 7 above, with a p-value of 0.570 higher than the level of significance (0.05), X1 (working capital/total assets) has no significant contribution to the model. This means that the ratio of working capital to total assets has no significant impact on banks' financial distress; hence it is not a better and more substantial predictor of bank distress.

Test of hypothesis 2: “Retain Earnings to Total Assets ratio is not a better and more significant predictor of distress

Comment/Interpretation: According to the Table 7 above, with a p-value of 0.002, which is less than level of significance (0.05), X2 (retain earnings to total assets) has a significant contribution to the model; hence it is said that the ratio retain earnings to total assets is a better and more substantial predictor of bank distress. The ratio has a negative relationship with the dependent variable. The implication is a unit increase in the ratio result in a decrease in the banks’ financial distress and verse visa.

Test of hypothesis 3: “EBIT to Total Assets ratio is not a better and more significant predictor of distress.”

Comment/Interpretation: As shown in table 7above, with a p-value of 0.002, which is less than the level of significance (0.05), therefore the null hypothesis is rejected at a 95% confidence interval. This implies that the ratio contributed significantly to the model, i.e., EBIT to total assets is a better and more significant predictor of bank distress.

Test of hypothesis 4: “Value of Equity to Book Debt ratio is not a better and more significant predictor of distress.”

Comment/Interpretation: From table 7above, it was found that the p-value (0.807) is more significant than level of significance (0.05); hence null hypothesis is accepted and then say that value of equity to book debt ratio (X4) has no significant contribution to the model, i.e., the value of equity to book debt ratio is not a better and more substantial predictor of bank distress.

Test of hypothesis 5: “Gross Earnings to Total Assets ratio is not a better and more significant predictor of distress.”

Comment/Interpretation: According to table 7 above, the p-value (0.002) is less than the level of significance (0.05); hence the null hypothesis is rejected at 95% confidence level. We then say that the ratio of gross earnings to total assets has a significant contribution to the model. That is, the gross revenues to total assets ratio is a better and more substantial predictor of bank distress.

Test of hypothesis 6: “The five ratios (Working Capital to Total Assets, Earnings to Total Assets, EBIT to Total Assets, Value of Equity to Book Debt and Gross Earnings to Total Assets) cannot be used in classifying the three banks (GT Bank, UBA and Polaris) into weak, strong and very strong banks.

Table 8: Banks’ Financial Rating Cross Tabulation

|

Count |

Financial rating | Total | ||||

| Weak | Strong | Very strong | ||||

| Banks | GT Bank | 0 | 6 | 18 | 24 | |

| UBA | 1 | 16 | 7 | 24 | ||

| Afribank | 4 | 5 | 15 | 24 | ||

| Total | 5 | 27 | 40 | 72 | ||

Source: SPSS 20.0 output

Table 9: Chi-Square Test

| Value | Df | Asymp. Sig. (2-sided) | |

| Pearson Chi-Square | 18.272a | 4 | .001 |

| Likelihood Ratio | 18.967 | 4 | .001 |

| Linear-by-Linear Association | 2.590 | 1 | .108 |

| N of Valid Cases | 72 |

Comment/Interpretation:

With reference to table 4.9above, since the chi-square analysis indicated that the p-value (0.001) is less than a level of significance (0.05); hence null hypothesis is rejected at a 95% confidence level. We can then say that the five financial ratios can be used to classify the three banks under investigation into weak, strong and very strong banks.

4.2 Discussion of Findings

Outcome of test on hypothesis 1:

In our present study, it was ascertained that “Working Capital to Total Assets ratio is not a better and more significant predictor of distress.” It was found that X1 (working capital/total assets) has no significant contribution to the model. That is, X1 is not a better and more significant predictor of bank distress.

The above result is a sharp contrast to that the earlier works of Winakor and Smith (1935) who in their attempt to verify the efficiency of ratios as predictors of the financial fortunes or misfortunes of firms in the early ’30s concluded that the ratio of net-working capital to total assets was the most accurate and consistent indicator with its decline ten years before the occurrence of financial difficulty.

Outcome of test on hypothesis 2

In our present study, it was ascertained that retained earnings to total assets ratio has a significant contribution to the model. The implication is that the ratio is a better and more significant predictor of bank distress and that a 62.967% change in X2 (retained earnings to total assets ratio) result to a unit change in banks' distress. This is contrary to the findings of Siems (1992), who opined that the single ratios measuring managerial efficiency such as operating income to operating expenses suffer from several limitations. However, they provide an overall measure of profitability, and they fail to indicate resource allocation and product decisions made by management because both the numerator and denominator are aggregate measures.

Outcome of test of on hypothesis 3

In our present study, it was ascertained that X3 (EBIT to total assets) contributed significantly to the model, i.e., EBIT to Total assets is a better predictor of banks’ financial distress. The implication is that 147.386% change in the EBIT to Total assets will result in a unit change in bank distress. This agrees with the findings of Mine Ugurlu (2006) that EBITDA/total assets is the most important predictor of financial distress in both models.

Outcome of test of on hypothesis 4

The present study indicates that the value of equity to book debt ratio does not significantly contribute to the model formulated for policymaking. The implication is that this ratio is not a better and more significant predictor of bank distress. These findings run contrary to the earlier works of Fitz Patrick (1931), who identified the ratio of Net-worth to Net debt and Net worth to fixed assets as the best predictors of a firm’s financial failure. Fitz Patrick (1931) used a relatively small sample in his research, which attracted criticism from other scholars.

Outcome of test of on hypothesis 5

In the present study, gross earnings to total assets ratio were found to have significant contribution to predicting financial distress in banks, i.e., gross earnings to total assets ratio is a better and more significant predictor of bank distress. The implication is that a 55.379% change in gross earnings to total assets ratio tends to a unit change in the bank financial distress. This study corroborated the earlier works of Adekanye (1993), where he adopted multivariable discriminate analysis (MDA) and logit regression techniques to test on bank distress. He confirmed that managerial efficiency is an overriding determinant of commercial bank performance in Nigeria. It is important to note that X3 and X5 are both measures of administrative efficiency.

Outcome of test of on hypothesis 6

The present study indicates that the p-value (0.001) is less than the level of significance (0.05). Thus, the null hypothesis is rejected at 95% confidence level. It is then agreed that the five financial ratios (X1, X2, X3, X4 and X5) can be used to classify the three banks under investigation into weak, strong and very strong banks.). This assertion supports the findings of Sexton (1992), who maintained that ambiguity makes ratio analysis ineffective in measuring actual efficiency. However, a combination of carefully selected ratios to form a model will serve as a useful tool for the prediction of corporate distress.

5. Summary, Conclusion and Recommendations

5.1 Summary

Failure prediction models are used extensively in the financial community for company evaluations and as early warning signs of potential business failure. Such models have been used by commercial banks and creditors to assess the creditworthiness of commercial users, by investors to measure a firm’s risk of insolvency and by business, managers to assess and manage the financial turnaround of distressed companies. The evolution of ratio analysis can be traced to the increasing need for financial information by professional managers for them to make appropriate decisions and measure the effectiveness of their utilization of the resources under their control. There is a need for business owners to attain more detailed information relating to returns, appraisals and other investments. However, the modern approach in the use of financial ratios involves the utilization of a combination of ratios with some statistical and mathematical techniques to construct a model with the ability to describe, indicate and, most importantly, predict the welfare of business organizations with significant accuracy.

5.2 Conclusion

A logistic regression analysis was conducted on financial data collected for this purpose. The task was to examine the relationship between financial distress and the various financial ratios. Five ratios were included in the study, and observations show that only three ratios, namely Retaining earnings to total assets ratio, earnings before interest and tax (EBIT) to total assets and gross earnings to total assets, were found to be significant predictors of bank distress.

5.3 Policy Implications

The result of this study points to the fact that financial statements of Nigerian banks have good information content that enables investors to monitor the health of banks and provide contribution at Annual General Meetings( AGM’s). It gives the regulatory authorities additional insight on how the logistic regression model can be used to improve their supervisory oversight function. With different techniques and tools of this nature, the banks can identify when essential financial data is signaling a change in direction and strategy, and this keeps the bank healthy and profitable. When the model signifies that a bank is weak, top management is advised to make business decisions that will boost profitability as this is the most crucial factor in predicting distress.

5.4 Recommendations

This study, therefore, recommends that:

- Management of commercial banks should focus more on their earning capacity as compared with their asset size as this is critical to long term survival.

- Regulatory authorities such as CBN and NDIC should intensify supervisory activities on banks to reduce the level of non-performing loans and risk assets possessed by banks. This will help boost the banks’ earnings and reduce the likelihood of distress.

- Global best practices in corporate governance should be maintained by bank management personnel.

- Further studies should be conducted on distress, particularly in other economic sectors.

References

- Adewumi, S. (1996). The Effects and Challenges of Financial Liberalization.

- Adeyemi, K. S. (2005). Banking Consolidation in Nigeria: Issues and Challenges, Union Digest, 9(3 & 4).

- African Economic and Business Review Vol. 6 No. 2, Fall 2008.

- African Economic and Business Review Vol. 6 No. 2, Fall 2008. ISSN 1109-5609 © 2008.The African Education and Business Research Institute, Inc. 43.

- Agusto & Co. (1995), Banking Industry Survey (Lagos). BERGER, Allen N., Richard J. HERRING and Giorgio P. SZEGO (1995), "The role of capital in financial institutions", Journal of Banking and Finance, Vol. 19, pp. 393-430. Crossref

- Akhavin, J. D., Berger, A. W., & Humphrey, D. B. (1997). The effects of mega mergers on efficiency and prices: Evidence from a bank profit function. Review of Industrial Organization: 12. Crossref

- Argenti, J. (1976), Corporate Collapse: The Causes and Symptoms, McGraw Hill, London

- Ayodele, A. (2005). Foreign Capital inflows: The gains, the pains. This Day.

- Beaver, William H., (1966). Financial Ratios as Predictors of Failure, Journal of Accounting Research, Supplement, Empirical Research in Accounting: Selected Studies, pp. 71-111. Crossref

- Beaver, William H., (1968a). Alternative Accounting Measures as Predictors of Failure, The Accounting Review, January, pp. 113-122.

- Beaver, William H., (1968b). Market Prices, Financial Ratios, and the Prediction of Failure, Journal of Accounting Research, Autumn, pp.179-192. Crossref

- Beck, T. A., Cull, R., and Jerome A. (2005). Bank privatization and performance: Empirical evidence from Nigeria, Journal of Banking and Finance, 14: 597-605. Crossref

- Benston, G.J. et`al (1986), Perspectives on Safe and Sound Banking: Past,PresentFuture

- Blum, M. (1974). Failing company discriminant analysis. Journal of Accounting Research, 12 (Spring): 1-25. Crossref

- Boyd, J. H. and Prescott, E. C. (1986). Financial Intermediary-Coalitions. Crossref

- BOZ (1995), Annual Report (Lusaka: Bank of Zambia). CAPRIO, Gerald, Jr. (1996), "Bank regulation: The case of the missing model", Policy Research WorkingPaper, No. 1574 (Washington, DC: World Bank). (1997), "Safe and sound banking in developing countries: We're not in Kansas anymore" PolicyResearch Working Paper, No. 1739 (Washington, DC: World Bank)

- Canbaş, S., Çabuk, A. and Kılıç, S.B. 2005. Prediction of commercial bank failure via multivariate statistical analysis of financial structures: The Turkish case. European Journal of Operational Research 166 (2), 528-546. Crossref

- Caprio, G., Jr., and Summers, A. H. (1993), "Finance and its reform" Policy Research Working Paper, No. 1171 (Washington, DC: World Bank).CBK (various issues), Annual Report and Accounts (Nairobi: Central Bank of Kenya).(1995), Monthly Economic Review (Nairobi: Central Bank of Kenya), November.

- Carlin, W. & Mayer, C. (2003). Finance, Investment and Growth, Journal of Financial Economics, 69(1). Crossref

- Charles W. Calomiris and Berry Wilson, 2004. "Bank Capital and Portfolio Management: The 1930s "Capital Crunch" and the Scramble to Shed Risk," Journal of Business, University of Chicago Press, vol. 77(3), pages 421-456, July. Crossref

- Collier, P. (1993), "African financial liberalisations", mimeo (Oxford: Centre for the Study of African Economies).

- De Long, J. Bradford. (1991). Did Morgan’s Men Add Value? An Economist’s

- Demirgüç-Kunt, Aslı; Detragiache, Enrica. 2005. Cross-Country Empirical Studies of Systemic Bank Distress : A Survey. Policy Research Working Paper; No. 3719. World Bank, Washington, DC. © World Bank Crossref

- Demsetz, R. S., SAIDENBERG, M. R. & Strahan, P. E. (1997), "Agency problems and risk taking at banks", Federal Reserve Bank of New York Research Paper, No. 9709 (New York). Crossref

- Diamond, D.W. (1984). Financial Intermediation And Delegated Monitoring, Review of Economic Studies, 51(3). Crossref

- Distribution of Income, Journal of Political Economy, 5(1).

- Ebhodaghe J.U. (1996), “Distress Management and Prevention Strategies for the Nigerian Banking System EIU (1995), Country Report Kenya, fourth quarter (Nairobi), Economist Intelligence Unit.

- Ekundayo, J. O. (1994). The Future of the Banking Industry in Nigeria, CBN Economic and Financial Review: 32(3).

- Fukuyama, H. (1993). Technical and Scale Efficiency in Japanese Commercial Banks: A Non-Parametric Approach, Applied Economics, 25: 1101-12. Crossref

- Garcia, G. (1996), "Deposit insurance: Obtaining the benefits and avoiding the pitfalls", IMF Working Paper, No. WP/96/83 (Washington, DC: International Monetary Fund). Crossref

- Glaessner, T. and Mas, I. (1995), "Incentives and the resolution of bank distress", The World Bank Research Observer, Vol. 10, No. 1 (February), pp. 53-73. Crossref

- Greenwood, and Jovanovic, B. (1990). Financial Development, Growth, and the Guaranty Trust Plc. (2008) Equity Research Report. A research publication of Greenwich Research Crossref

- Harvey, C. and Jenkins, C. (1994), "Interest rate policy, taxation and risk", World Development, Vol. 22, No. 12, pp. 1869-1879. Crossref

- Harvey, C. (1993), "The role of commercial banking in recovery from economic disaster in Ghana, Tanzania, Uganda and Zambia", IDS Discussion Paper, No. DP.325 (Brighton: Institute of Development Studies, University of Sussex).

- Heiko, H. (2007). Financial Intermediation in The Pre-Consolidated Banking Sector. In Nigeria, World Bank Policy Research Working Paper No. 4267 June.

- Helfert, Erich A.Techniques of Financial Analysis: A Modern Approach. 9th ed. Chicago: Richard D. Irwin, Inc., 1997.

- Hellmann, T., Murdock, K and Stiglitz, J. (1995),"Financial restraint: Towards a new paradigm", Research Paper, No. 1355 (Stanford: Graduate School of Business, Stanford University).

- Ikhide, S.I. (1996), "Financial sector reforms and monetary policy in Nigeria", mimeo (Brighton: Institute of Development Studies, University of Sussex)

- Imala, O. I. (2005). Consolidation in the Nigerian banking industry: A strategy for survival and development. A paper presented during the visit of the Nigerian economics students association (NESA), University of Abuja chapter.

- James H. Bliss, Financial and Operating Ratios in Management (The Ronald Press Company, 1923), pp. 34-38

- Kariuki, P. W. (1993), "Interest rate liberalisation and the allocative efficiency of credit: Some evidence from the small and medium scale industry in Kenya", Ph.D. thesis (Brighton: Institute of Development Studies, University of Sussex).

- Kwan, S. (2004). Banking Consolidation Federal Reserve Bank of San Francisco

- Lemo, T. (2005).Regulatory Oversight and Stakeholder Protection. A Paper Presented At the BGL Mergers and Acquisition Interactive Session, Held at EKO Hotels and Suits Victoria Island, June 24.

- Lewis, P., and Stein, H. (1997). Shifting Fortunes: The Political Economy of Financial Liberalization in Nigeria.World Development, 25: 5-22. Crossref

- Lewis, Peter and Howard STERN (1997), "Shifting fortunes: The political economy of financial liberalisation in Nigeria", World Development, 25 (1), pp. 5-22. Crossref

- Mamman, H. and Oluyemi, S.A. (1994), "Bank's management issues and restoring the health of the economy

- Manu, B. (1994), "Critical issues to consider when establishing a deposit insurance scheme", Nigeria Deposit Insurance Corporation Quarterly, 4 (3), pp. 13-32

- Mckillop, D., Glass, J. C., and Morikawa, Y. (1996). The Composite Cost Function and Efficiency in Giant Jappanese Banks.Journal of Banking and Finance, 20: 1651-71.McKinnon, R. I. (1988), "Financial liberalisation in retrospect: Interest rate policies in LDCs", in Ranis, Gustav and T. Paul Shultz (eds.), The State of Development Economics: Progress andPerspectives, New York: Basil, Blackwell, pp. 386-410. Crossref

- Mine Uğurlu, Hakan Aksoy, (2006) "Prediction of corporate financial distress in an emerging market: the case of Turkey", Cross Cultural Management: An International Journal, Vol. 13 Issue: 4, pp.277-295. Crossref

- NDIC (various issues), Annual Reports, Lagos: Nigeria Deposit Insurance Corporation.

- Nigerian banks through improving the quality of management/employees", Nigeria Deposit Insurance Corporation Quarterly, 4 (4), pp. 56-70.

- NSE (1995-2014). Fact Book Nigerian Stock Exchange.

- Nwankwo, G.O. (1980), The Nigerian Financial System, London: Macmillan.

- Nwezeaku N. C. (2006), Financial Management

- Oboh, G. A. T. (2005). Selected Essays on Contemporary Issues in the Nigerian Banking System, Ibadan University Press.

- Okeke, E. (2006). Effects of the Recapitalization on the Nigerian Economy, Sun News January 21.

- Olaniyi, T. A. (2007)Predicting potential of failure in Nigerian banking sector: A Comparative Analysis of First Bank Plc and Trade Bank Plc. Babcock Journal of Management and Social Sciences 6 (1), 64-73

- Olisadebe, E.U. (1991), "Appraisal of recent exchange rate policy measures in Nigeria", Central Bank of Nigeria Economic and Financial Review, 29 (2), pp. 156-185.

- Oluajakaiye, P. (1995). Short Run Macroeconomic Effects Of Bank Lending Rates In Nigeria 1987-1991, AERC Research Paper, 34 Nairobi Kenya.

- Otangaran, I. (2004). Stakeholders Perspective on the N25 billion capital base, Financial Standard, 5(40).

- Pandey I. M. (2003). Financial Management, Vikas Publishing House, 2003.

- Pandey I. M. (2004). Financial Management, Vikas Publishing House, 2004.

- Perspective on Finance Capitalism, in P. Temin (Ed.), The Business Enterprise: Historical Perspectives on the Use of Information, Chicago: University Of Chicago Press: 205-36.

- Popiel, P. A. (1994). "Financial systems in sub-Saharan Africa: A comparative study", World Bank Discussion Paper, No. 260, Washington, DC: World Bank.

- Sanusi, L. S.(2010). “The Nigerian Banking Industry: what went wrong and the way forward”. Being the full text of a Convocation Lecture delivered at the Convocation Square, Bayero University, Kano, on Friday 26 February, 2010 to mark the Annual Convocation Ceremony of the University)

- Sirri, E. R., and Tufano, P. (1995). The Economics Of Pooling in The Global Financial System: A Functional Approach. Eds. Dwight B. Crane, Et Al., Boston, MA:Harvard Business School Press. African Economic and Business Review 6 (2), Fall 2008. ISSN 1109-5609 © 2008 The African Education and Business Research Institute, Inc. 45

- Sloan, H., and Zurcher, A. (1970). Dictionary of Economics, New York: Barnes and Noble Books.

- Smith and Arthur H. Winakor, Changes in the Financial Structure of Unsuccessful Industrial Corporations, University of Illinois, Bureau of Business Research, Bulletin No. 51, 1935, p. 8.

- Soludo, C. C. (2004). Consolidation and Strengthening Of Banks, Speech Delivered At the Meeting of Bankers Committee 6th August 2004.

- Soyibo A. and Adekanye, F.(1992),”The Nigerian Banking System in the Context of Policies of Financial Regulation and Deregulation” AERC Research Paper Seventeen, African Economic Research Consortium (AERC), Nairobi, December.

- Stiglitz, J. E. and Weiss, A. (1981), "Credit rationing in markets with imperfect information", American Economic Review, Vol. 71, pp. 393-410.

- Sundararajan, V. "Banking Crisis and Adjustment: Recent Experience." IMF Central Banking Seminar Papers. Washington D. C.: International monetary Fund, December 1988

{kind=link}