International Journal of Management Science and Business Administration

Volume 10, Issue 2, January 2024, Pages 7-14

The Functions of the Brazil Federal Court of Accounts in the Improvement of Public Administration

DOI: 10.18775/ijmsba.1849-5664-5419.2014.102.1001

URL: https://doi.org/10.18775/ijmsba.1849-5664-5419.2014.102.1001 Hugo Leonardo Menezes de Carvalho.

Hugo Leonardo Menezes de Carvalho.Accounting Department, Ceuma University, Sao Luis, Brazil

Abstract: This article aims to analyze the control benefits exercised by the Brazil Federal Court of Accounts - TCU to improve Public Administration, considering that an extensive range of studies has been developed on public efficiency, but without considering the aspect of control as an essential instrument of this transformation, and also by the fact that the Federal Executive Power has sometimes exposed the TCU as an impediment to the development of the country From a methodological approach qualitative, exploratory, with the use of literature and document analysis, the barriers to an efficient public administration and the functions performed by the TCU were analyzed. Thus, it was evidenced that public efficiency can be achieved by tackling impediments to an efficient model identified in this article by two groups: the Legality of deviations and purpose and improper operation. From this identification, the type of control exercised by TCU was presented according to its legal powers, the focus of its operations, and the resulting benefits, which were also presented in financial and operational groups. Thus, it was concluded that the benefits generated by TCU's actions work in fighting impediments to efficient public Administration, consequently contributing to improving the federal public Administration.

Keywords: Brazil Federal Court of Accounts, Improvement, Public Administration

1. Introduction

Administration is a Science that consists of a particular combination of elements to achieve a specific objective (Taylor, 1990). With this, Public Administration constitutes an essential segment of administrative Science. It represents the State's equipment and the form of Government to plan, organize, direct, and control its administrative actions to provide total and complete satisfaction of basic collective needs. As the government sector constitutes a specific organizational form and considering the presence of a democratic Republican State based on the rule of law, in the Brazilian case, in which public managers are bound by the legal commandments of an administrative, legal regime, the need to remodel the means of control emerged between society and governments.

Thus, given the peculiarities of the public sector, such as the administrative, legal regime, and bureaucratic form of organization, it ends up highlighting the controlling aspects that exist in this branch, especially since the legal nature of control is that of a fundamental principle of Public Administration, and must be exercised, therefore, at all levels of state administrative power (Carvalho Filho, 2007). In the same vein, the democratic rule of law, adopted by the Brazilian system, requires control mechanisms that can be exercised by agents that are outside the administrative structure and that are, so to speak, totally unrelated and impartial to the activity that will be the object of control (Castro, 2007).

Despite this emphasis on the control function applied to public Administration, its role in achieving the desired public results must be analyzed in greater depth needs to be analyzed in greater depth. It needs to be more precise with bureaucracy, unnecessary obstacles, and the target of managers' opinions. Public groups against specific control actions, which, in their opinion, do not contribute to management efficiency, a fact that renews the field of possibilities to develop discussions on the role of control in Administration amidst the significant growth of its activities, notably with the implementation of structuring programs, applied nationally, and which add to the already complex state activities.

Therefore, the present work is justified by the topicality and relevance of the topic in the Context of Brazilian public Administration and its relationship with existing controls. Notwithstanding the considerations about the presence of control in Public Administration, it is necessary to highlight how this control can be exercised. Therefore, Administration control is a genre from which we can extract several species, with no definitive classification, but presenting itself as internal, external, and social control (Guerra, 2011). Regarding external control, as taught by Guerra (2011), the Audit Courts will act independently, with their duties, exercising external Power of the public Administration whose product of this action is intended to assist the Legislative Branch. Given this scenario, interest arises in analyzing the performance of control, especially the external control exercised by the Federal Audit Court (TCU). This leads to the research problem of the present work: What is the role of the TCU in improving Public Administration Federal?

To this end, the main objective is to analyze the benefits of the control exercised by the TCU to improve the Federal Public Administration, considering that an essential range of studies has been developed on public efficiency, but without considering the aspect of control as a necessary instrument of this analysis. In this way, the study aims to elucidate the supposed dichotomy between efficient public management and external control exercised by the TCU, demonstrating the factors impeding the improvement of the Federal Public Administration – APF, with the functions performed by the TCU, based on a methodological approach of qualitative, exploratory nature, with the use of bibliographical research and documentary analysis, whose focus of interest is, therefore, the federal public Administration and the external control exercised by the Federal Audit Court.

Therefore, considering the main objective of the research and the vast field of activity of the Federal Court of Auditors within the scope of Public Administration, the specific goals are the presentation of the legal powers of the TCU and the identification of factors impeding public efficiency in comparison with the benefits to the APF resulting from the TCU's actions. With this, a critical examination is developed on the role of the TCU in improving the APF, especially regarding how the Court operates and the possible benefits and consequent contribution to improving public Administration and strengthening the external control function in the APF, providing greater transparency and effectiveness of government action.

2. Literature Review

2.1 Efficient Public Administration

Public Administration is an aspect of a more general concept; Administration is responsible for studying the means necessary to achieve certain ends. In a more restricted sense, it indicates that Public Administration is the management of qualified assets and interests of the community at the federal, State, or municipal level, according to the precepts of Law and Morals, aiming for the common good (Meirelles, 2005). Thus, the Administration is the Government's instrument, comprising legal entities, bodies, and agents encompassing its activities. From the concepts of public Administration, much was dedicated to studying its forms, compiling specific characteristics about the modes of Administration or administrative periods in which the so-called theories of public Administration were constructed.

Along these lines, Zwick et al. (2012) observe that patrimonialism, bureaucracy, and managerial public Administration were the three predominant models in the Brazilian case over time. We need to detail the respective definitions and characteristics of each of these models in which scholars usually align Brazilian Public Administration, or else we have, in concrete terms, an attempt to change the form of Administration to achieve a particular purpose in a certain way. Therefore, knowing why each administrative form is adopted is more than didactically presenting administrative theories. Regarding this administrative evolution, he expresses that the conceptions regarding Public Administration are progressively evolving towards the idea of an efficient State (Andion, 2012). The same line is pointed out by Gomes (2009), who highlights the concern of public administrations with the search for the efficiency of public policies and services as being a common axis in any administrative perspective.

It is noted that the primary and common issue discussed in the various administrative theories refers to examining how Administration can be efficient in what it proposes. In this way, the concept of efficiency can be generalized as that related to using resources to obtain the best cost-benefit relationship between the established objectives and the resources used (Gomes, 2009). Thus, efficiency is a characteristic that every administrator needs to observe so that the expected positive results can be achieved without wasting the means necessary actually to achieve the desired objectives. Since efficiency is an intrinsic characteristic of any Administration, in the public sector, it could not be different, and, in the Brazilian case, it was established in the caput of article 37 of the Constitution of the Republic as a constitutional principle of Public Administration. However, this was already mentioned in the infraconstitutional legislation, such as Decree Law no. 200/67 (articles 13 and 25, item V). In the case of the public sector, efficiency means meeting the community's needs in the best possible way, given the means available to achieve positive and satisfactory results. Along these lines, Meirelles (2005) argues that the Principle of efficiency requires that administrative activity be carried out with speed, perfection, and functional performance. It is the most modern Principle of the administrative function, which is no longer content to perform only legally, demanding positive results for the public service and satisfactory fulfillment of the community's and its members' needs. (Meirelles, 2005, p. 96).

Custódio Filho (1999) adds that efficiency involves three ideas: helpfulness, promptness, and economy. Thus, efficiency derives from the search for adequate service to citizens and their demands, with the agility and organization necessary for the best use of available resources and the permanent concern to achieve the maximum of intended objectives, even with limitations. To this end, it instigates changes in processes and procedures so that work routines can adapt to society's demands without compromising the expected results. Lopes (1998) contributes by expressing the understanding that nothing is efficient in Principle but in consequence. Therefore, according to the same author, Public Administration will not be efficient if problems such as deviations observed in it persist. Consequently, it is admitted in this work that an Administration, regardless of its sphere or doctrinal framework, exists to offer the best possible return given its limited resources. Hence, this macro objective is only possible when the so-called impeding factors to Efficiency do not exist. Public.

2.2 Factors Impeding Efficient Public Administration

According to Bresser-Pereira (1998), efficient Public Administration refers to a new articulation of relations between Society and State, which aims to combat the capture of the State by private interests, defend public assets, and use scarce public resources—taxpayers, to meet the general welfare, its primary objective. In general, comparing the contribution of Bresser-Pereira (1998), two large groups of factors that impede an efficient governmental administrative model can be identified: the fight against the use of public assets for private interests and the efficient application of resources for achieving your objectives. Thus, when conduct and actions do not match the intended legal objective, there is a deviation that may be a deviation from Legality due to non-compliance with Laws and norms or deviation from Purpose, conceptualized by Meirelles (2005) as meeting the purposes of general interests, total or partial renunciation of powers or competence is prohibited unless authorized by law. Regarding this aspect, it is noted that the goal of Public Administration is to solve or deliver to society a product expected by it or a solution to a problem complained about.

So, it is possible to identify that one of the groups of factors impeding efficient public Administration is represented by deviations from Legality and purpose. Emphasizing, in this case, that this generalization proposed here does not invalidate the fact that factual situations of non-compliance with the law did not exist precisely to demonstrate a more efficient administration, this is because the concept of Legality should not stick only to the literality of the norm whose content it is unable to regulate the different circumstances in the different spheres of public Administration. This is because, as Rocha (2002) emphasizes, not every act of mismanagement constitutes an illicit act, which requires prolonged demonstrations of responsibility for the sake of legal certainty. On the contrary, every enterprise, even those sponsored by public authorities, involves risks. Minimizing the harmful effects of decisions that prove wrong requires prompt action from the control system, understood as an input to the decision-making process (Rocha, 2002).

Therefore, the characterization of a deviation from Legality or purpose must also include the material truth and the legitimacy of the action by the spirit of the norm about its practical application. A second group of factors impeding efficient public Administration could be called inadequate operations, as there is no gain in the relationship between resources spent and the results achieved. Efficiency refers to how and processes the organization approaches problems (Gomes, 2009). The precarious management conditions of Brazilian public organizations are a reflection of this framework of institutional discontinuity, combined with the predominantly bureaucratic and procedural character that regulates the exercise of public Administration, the inadequate managerial profile of occupants of trust functions, and the low instrumental condition of public Administration Brazilian, about operational technology, methods, and processes. This situation of precariousness constitutes a factor of inefficiency and ineffectiveness, decisively affecting the rationality of implementing public policies (Martins, 1995). On this basis, the largely predominant findings on efficiency refer, for the most part, to management systems and practices and, sometimes, to the work environment (Albuquerque, 2006). In other words, they deal with flaws in procedural flows or administrative structuring related to the operation of public entities, which will prevent the expected objectives from being achieved, preventing efficient action.

With this logic, inadequate operation presents itself as a relevant reason in the Context of efficiency because more than a confluence between means and ends or just a focus on results, contemporary times require a set of these concepts to reveal the desire for an Administration effective public sector, that is: one that not only does not waste its scarce resources but also produces and presents quality results for its population. In this way, it is evident that the factors impeding efficient public Administration attack several areas of administrative insertion, from the legal to the operational, being, therefore, a complex set. Still, despite this, it can be compiled into 2 (two) large groups of factors: Deviations from Legality and Purpose and Inadequate Operation. From this identification, it becomes possible to understand the measures that can be adopted to avoid materializing these factors and contribute to improving management. In this case, the role of control in this context will be analyzed, particularly the external control exercised by the Federal Audit Court.

3. Control Exercised by the Federal Audit Court

The concept of organizational control in its complete form reflects the means management uses to create patterns of behavior to be followed by organizational members (Nascimento and Reginato, 2009). As the government sector constitutes a specific organizational form, the applicability of control mechanisms will provide functionality similar to that practiced in the private sphere but with the adjustments pertinent to the public sector since the State is permanently related to society, and From these relationships arise its functions, linked to one of the fundamental functions: executive, legislative or legal. In this way, the State submits itself to order and administrative efficiency. These principles create mechanisms or systems for controlling state activities and defending public Administration and collective rights and guarantees. This emphasis on the control function applied to Public Administration has, in addition to the legal character that establishes it, the supervisory focus of society on the actions of public managers to prevent them from acting in the name of private interests, theirs or those of others. Then, the peculiarities of the public sector, such as the administrative legal regime and the bureaucratic form of organization, will enhance the aspects of control in this sector. It is precisely through management that those administered and the Administration can assess the legitimacy or convenience of administrative conduct. For this reason, this possibility reflects, without the slightest doubt, a guarantee for both (Gasparini, 1992). It also adds that the legal nature of control is a fundamental principle of Public Administration. It cannot be waived or refused by any administrative body and must be exercised at all levels of Power (Carvalho Filho, 2007). Despite these understandings regarding control in Public Administration, it is necessary to understand that there are different forms of control. Administration control is a genre from which we can extract several species with no definitive classification (Guerra, 2011).

In this sense, control can be internal or external. As for the body that executes it, it can be administrative, legislative, or judiciary and is carried out previously, concomitantly, and a posteriori, involving aspects of Legality and merit ( Mileski, 2003). That is why the modality called external control gained prominence, under the responsibility of the Legislative Power, a worthy representative of the people in the spheres of Power, and that, as the Legislative Power did not have all the necessary conditions for the solitary exercise of this attribution, it became necessary to create a specialized technical body that could assume part of the competencies inherent to control (Guerra, 2011). Thus, it is possible to understand that the competencies developed by the Federal Audit Court – TCU, as well as the benefits arising from this action, result from the presence of control in the Brazilian Federal Public Administration, more specifically, the exercise of external Power, which has as its characteristic fundamental that it is performed by a body outside the structure of another controlled entity, seeking to implement mechanisms to guarantee the full effectiveness of government management actions. (Guerra, 2011).

3.1 Focus on External Control Carried out by the TCU

The exercise of external control carried out by the TCU gained new contours, primarily related to the evolution of government actions and the collective's desires, now more focused on the results of spending than on the legal technicalities affected by the execution of public resources. Public Administration control must observe not only the aspect of Legality but also the result of public action, checking whether they were helpful enough for their intended purpose (Figueiredo, 2000). Thus, what was previously restricted only in terms of formal aspects now also acquires a new form, questioning acts and policies regarding their economicity, effectiveness, and results. The demands for better services and the search for economy and energy in using public resources have guided the actions of citizens, who have progressively been demanding transparency, honesty, morality, and excellence in Public Administration. For these reasons, in exercising its constitutional role, the TCU has focused on inspections focused on the performance of the audited entity and the efficiency, effectiveness, and effectiveness of government actions (Santos, 2003).

Therefore, Audits, despite being just one of the TCU's instruments of action, it is the most significant way in terms of performance and results, and which, according to the TCU's Auditing Standards (2010, p. 14), are classified regarding nature, in Regularity audits: aim to examine the Legality and legitimacy of the management acts of those responsible subject to the jurisdiction of the Court, regarding accounting, financial, budgetary and patrimonial aspects. Regularity audits comprise compliance audits and accounting audits. Operational audits aim to examine the economy, efficiency, and effectiveness of organizations, programs, and government activities to evaluate their performance and promote the improvement of public management.

It should be noted that the Legality of management acts and public performance in terms of economy, efficiency, and effectiveness are examined. However, the discussion under the focus of public control, especially on the part of those controlled, does not reflect the evolution and essentiality of this administrative function, so it is usually associated with obstacles to a bureaucratic model of Administration, as Gomes (2009) reveals: A fourth point in this argument about issues that can influence the efficiency of the State refers to bureaucracy. The possibility of isolating politics from bureaucracy in such a way that the problem of efficiency would be limited solely to the political sphere, given the efficiency inherent in the concept of Weberian bureaucracy, is challenged by the politicization of bureaucracy itself and by other dysfunctions that compromise its efficiency (Gomes, 2009). This perception of bureaucracy influences public managers' thinking in the sense of unduly intertwining dysfunctions of the bureaucratic system with the role of control in the organization. This can be seen when public managers attribute authority as a possible cause of an inadequate operation without considering the fundamental role to be played by control and its function in improving public management. In this sense, a false dilemma emerges that administrative efficiency does not need control and that control is an ineffective obstacle. Examining the benefits of control compared to the factors impeding public efficiency is essential, enabling a more complete analysis of control's fundamental role.

4. Research Methodology - Materials and Methods

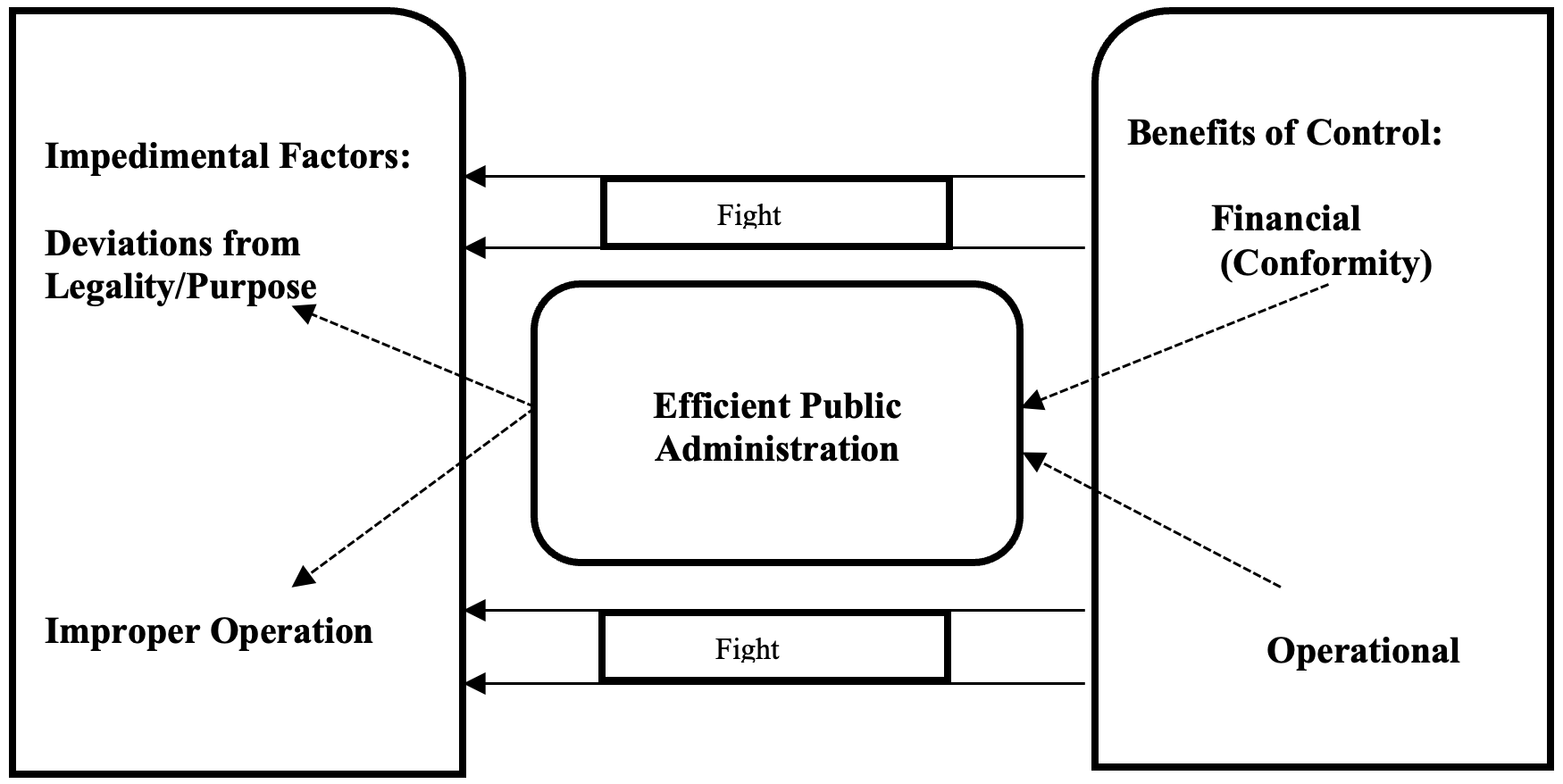

For the analysis of this supposed dichotomy between control and public efficiency and compliance with the general objective of this work of analyzing the benefits of Power, specifically that exercised by the Federal Audit Court – TCU, for the improvement of Federal Public Administration, the methodological approach, in relation The research process adopted was qualitative, since this approach is more subjective and involves examining and reflecting perceptions to obtain an understanding of social and human activities (Collins and Hussey, 2005). Regarding the objectives, this is an exploratory type of research, given the scarcity of studies on the research problem (Collins and Hussey, 2005), and the technical procedures adopted in this work were bibliographical research and document analysis to highlight legal competencies of the TCU, as well as to gather the theoretical elements required to understand the meaning of efficient Public Administration and its compatibility with the benefits of external control arising from the actions of the Federal Audit Court to improve Federal Public Administration. In this way, although the present work did not use numerical relationships or statistical inferences, the proposed research results can be reached, notably the relationship between control benefits and public efficiency, which can be summarized in Figure 1.

Figure 1: Impedimental Factors versus Benefits of TCU Control.

This way, you can highlight the results obtained. Without detailing the behavioral or psychological aspects of the agents involved, the central theme to be reinforced is that deviations from Legality and purpose, as well as inadequate operation, constitute factors impeding the presence of an efficient Public Administration and that, in this scenario, the financial benefits generated by the Federal Court of Auditors are presented as ways of combating these impeding factors. This is because compliance verification aims to prevent deviations from Legality and purpose, while operational actions aim to indicate weaknesses to be improved in an inadequate operation. Hence, it is incompatible to consider that the control and, therefore, the TCU's actions over the acts of political agents and public administrators could be the reason for an inefficient State; on the contrary, it should be seen as an element of contribution to the improvement of Administration Public Administration, thus functioning as an essential security barrier for the public administrator himself (Vieira, 2009).

5. Results and Discussion

As already explained, current control is aligned with the efficiency of government action. Another meaning can be extracted from this new constitutional Principle by combining it with art. Seventy of the constitutional text deals with the control of the Court of Auditors (Figueiredo, 2000). The teachings of Bresser-Pereira (1998) can be added, as the author cites the current tendency to provide greater flexibility to bureaucratic rigidity, incorporating practical and theoretical advances achieved by the private sector, such as the transition from procedural control to the control of results, maintaining, however, the final particularity of the State in serving the public interest.

It is noted that control is closely associated with management and, consequently, with understanding the role of Power. The absence of this perception on the part of Brazilian public managers already denotes the difficulty of establishing that control is a fundamental stone in improving management rather than an obstacle. Although authorities have always existed and were conceived as essential in the private sphere, including in a rigorous manner, since the search for return on investment is unavailable in that area, the same is not evident in the public sphere. This fact led to the development of forms and instruments of control, given the inertia of management itself (Cruz, 2009). In this way, control over the actions of rulers involves a double dimension: on the one hand, the sanction for possible deviant behavior; on the other, the judgment regarding his performance as a public manager. Therefore, although there are possibilities for improving performance, curbing excesses, or other improvements, the use of control instruments available to the TCU will generate, in some way, a type of administrative benefit, which is not possible when omission or negligence in the exercise of external control (Melo, 2007).

The fact is that the actions carried out by the TCU, in the general context, present benefits for the federal public Administration, and although the present work does not delve into the nuances of each control action developed to determine the individual effectiveness of the inspections, It is not the weakening of control that is the path to a better Public Administration, but rather its strengthening. Otherwise, one would admit that not carrying out external control was more beneficial than its implementation. These benefits can be considered and classified into financial compliance and operational. The financial benefits of compliance are those measurable or estimable in currency, in the case of debt convictions and fines in which the values are known, referring to actions that aim to curb and punish the practice of illegality. Operational benefits result from the assessment carried out in the main dimensions of the performance of a public organization, namely: economy, efficiency, effectiveness, and effectiveness of organizations, programs, and government activities, to seek to improve public management, resulting in direct effects on public efficiency and on the control itself that acts on the causes and not just the consequences. This action has directed external control towards analyzing corporate governance applied to the public sector, driven by a control body and not by the Administration itself.

6. Conclusion

From the above, the central objective of the work can be achieved, demonstrating the role of the Federal Audit Court - TCU in improving Federal Public Administration, adding the control function to the discussion about efficiency in Public Administration, since control, In addition to highlighting the actions carried out about the results achieved, it allows an assessment of what was planned, thus contributing to improved management. In this scenario, it was identified that efficiency, as a purpose to be achieved by the Administration, especially that related to the public sector, is not verified, in itself, by the presence of the Principle of Efficiency carved out in the Constitution of the Republic, but rather by the combating factors impeding an efficient governmental administrative model, summarized and identified by two groups, namely: deviations from Legality and purpose and inadequate operation.

From this identification, it was possible to understand that efficiency will be achieved if these factors are avoided. This is why the external control exercised by the TCU, through its legal and constitutional powers, is presented as an instrument to combat impeding factors. At that time, two considerable control benefits were highlighted: financial and operational. In this sense, control has been demonstrated as an integral and essential part of any process of producing goods and services whose primary function must be the search for better results by the organizations it integrates and must act in the various stages of the management process, detecting deviations and anomalies in a time compatible with the timely introduction of improvements and corrections that are necessary.

It is demystifying the control-bureaucratic obstacles relationship that corresponds to a kind of administrative common sense in the sense that the presence of controls is equivalent to a lack of management efficiency, which is why, not infrequently, there are manifestations that the TCU, in its responsibilities, ends up hindering national growth when it imposes sanctions or regulations on the Federal Administration. Public managers do not identify or do not seem to want to demonstrate that they know that not only the operational benefits contribute to better management, but also the financial benefits derived from compliance and that affect the manager's sphere in response to his actions or lack thereof, which is why These benefits, essential for the society that holds public resources, are not seen in this light, but instead as an undue or just legalistic sanction, without concern for improving management.

This perception reinforces the need for more synergy between control and public administrators. This distance ended up building a barrier between administrators and TCU so that their vision reflected something other than what the latter intended. Where there should have been a union of efforts, there was resistance. This situation requires a change in conception in which the role of control is clarified, as it occurs in the most competitive and efficient institutions so that the problem is not the presence of control, which represents a pillar and intrinsic function of any Administration, public or private, orthodox or organic. Still, the forms of power and control criteria need to be adapted to the various public functions. Indeed, the worsening of the control function is not desired and could lead to the mechanism of classical scientific management applied without distinction, where managers would be machines and not strategic leaders, when the ideal is a relativistic approach in which there are different forms of control suited to each activity. or relevant State task, such as turning to concepts hitherto not applied by the public sphere, such as the focus on results.

With this, it can be concluded that the benefits generated by the actions of the Federal Audit Court, financial and operational, result precisely from the effective exercise of its powers that aim to combat the factors that impede an efficient Public Administration, such as deviations in Legality and purpose and inadequate operation, which, consequently, demonstrates the role of the TCU in contributing to the improvement of federal public management.

References

- Albuquerque, Frederico de Freitas Tenório. (2006). Operational auditing and its challenges: a study based on the experience of the Federal Audit Court. 153f. Dissertation (Professional Master's Degree in Administration) – School of Administration, Federal University of Bahia, Salvador.

- Andion, Carolina. (2012). For a new interpretation of paradigm shifts in public Administration. Cad. EBAPE.BR, 10 (1), 01-19. CrossRef

- Constitution (1988). Constitution of the Federative Republic of Brazil. Brasília, DF, Senate, 1988. Internal Regulations of the Federal Audit Court. Bulletin of the Federal Audit Court. Special Edition. Brasília, DF, year 2012, n. 1, 2 Jan. 2012.

- Federal Audit Court. Operational audit manual. 3rd ed. Brasília: TCU, Secretariat for Inspection and Evaluation of Government Programs (Seprog), 2010.

- Federal Audit Court. Ordinance-TCU No. 280, of December 8, 2010. Approves the auditing standards of the Federal Audit Court (NAT). Bulletin of the Federal Audit Court, Brasília, DF, year XXLIII, n. 29, 10 Dec. 2010. Available at:

- Bresser-Pereira, Lc. (1998). State Reform for Citizenship. 1st ed. São Paulo: Editora 34.

- Carvalho Filho, José dos Santos. (2007). Administrative Law Handbook . 17. ed. Rio de Janeiro: Lumen Juris.

- Castro, Rodrigo Pironti Aguirre de. (2007). Internal control system: a perspective of the Public Managerial management model. Belo Horizonte: Forum.

- Collins, Jill; HUSSEY, Roger. (2005). Management Research: a practical guide for undergraduate and postgraduate students. 2nd ed. Porto Alegre: Bookman.

- Custódio Filho, Ubirajara. (1999). Constitutional Amendment 19/98 and the Principle of Efficiency in Public Administration. In: Notebooks on Constitutional Law and Political Science. São Paulo: Revista dos Tribunais, 27, 210-217.

- Di Pietro, Maria Sylvia Zanella. (2004). Administrative law. 17. ed. São Paulo: Atlas.

- Figueiredo, Lucia Vale. (2000). Administrative Law Course. 4th ed. São Paulo: Malheiros.

- Gasparini, Diógenes. (1992). Administrative law. São Paulo: Saraiva.

- Gomes, Eduardo Gomes Magalhães. (2009). Management by Results and Efficiency in Public Administration: an analysis of the Minas Gerais experience. Thesis presented to the Doctoral Public Administration and Government Course at FGV/EAESP.

- Guerra, Evandro Martins. (2011). External and Internal Controls of Public Administration. 2nd ed. rev. and ampl. 2. reprint. Belo Horizonte: Forum.

- Lopes, Maurício Antônio Ribeiro. (1998). Comments on the Administrative Reform: by Constitutional Amendments 18, of 02/05/1998, and 19, of 06/04/1998. São Paulo: Revista dos Tribunais.

- Martins, Humberto Falcão. (1995). The Modernization of Brazilian Public Administration in the Context of the State (Masters dissertation). Rio de Janeiro: Brazilian School of Public Administration of Fundação Getúlio Vargas.

- Meirelles, Hely Lopes. (2005). Brazilian Administrative Law. 31. ed. São Paulo: Malheiros.

- Melo, Marcus André. (2007). External Control in Latin America. Preliminary version for internal discussion. 2007. São Paulo: Instituto Fernando Henrique Cardoso.

- Mileski, Hélio Saul. (2003). Public Management Control. São Paulo: Revista dos Tribunais.

- Nascimento, Auster Moreira; REGINATO, Luciane. (2009). Controllership: A focus on Organizational Effectiveness. São Paulo: Atlas.

- Rocha, Carlos Alexandre Amorim. (2002). The External Control Model exercised by the Audit Courts and the legislative proposals on the subject. Brasília: Senado Federal, Consultoria Legislativa.

- Santos, Jair Lima. (2003). Federal Audit Court & State and Social Control of Public Administration. Curitiba: Juruá.

- Taylor, Frederick W. (1990). Principles of Scientific Administration. Translated by Arlindo Oliveira Ramos. 8. ed. São Paulo: Atlas.

- Vieira, Roberto de Araújo. (2009). The importance of internal control in a modern view of Administration and Finance at the State University of Rio de Janeiro. Rio de Janeiro.

- Zwick, Elisa et al. (2012).Tupiniquim public administration: reflections based on Theory N and Theory P by Guerreiro Ramos. Cad. EBAPE.BR, Rio de Janeiro, 10 (2). CrossRef

{kind=link}