International Journal of Management Science and Business Administration

Volume 6, Issue 4, May 2020, Pages 7-21

Financial Leverage on Earnings Management of Quoted Manufacturing Companies in Nigeria

DOI: 10.18775/ijmsba.1849-5664-5419.2014.64.1001

URL: http://dx.doi.org/10.18775/ijmsba.1849-5664-5419.2014.64.1001

1 Ogiriki Tonye (PhD), 2 Iweias Seth Sokiri (M.sc)

1 Associate Professor, Department of Accountancy, Niger Delta University, Bayelsa State, Nigeria

ogirikitonye@gmail.com

2 Department of Accountancy, Niger Delta University, Bayelsa State, Nigeria

iweias2013@gmail.com

Abstract: This study investigated financial leverage on earnings management in manufacturing firms in Nigeria. A total of twenty-nine (29) listed firms on the Nigeria Stock Exchange (NSE) were studied, and secondary data were extracted from their annual financial statements as reported in the factbook. Ordinary least squares (OLS) method was used to analyze the data. The results revealed that: the management of manufacturing companies in Nigeria employs all the three strategies of earnings management in their companies. The relationships between financial leverage and each of the dependent variables are positive but weak. Financial leverage does not have a significant impact on accruals earnings management in listed manufacturing firms in Nigeria; but it does on real earnings management and deferred tax earnings management; The study concludes that financial leverage has a positive impact on accrual earnings management, while both financial leverage and total leverage has a negative effect on real earning management. The study recommends that users of financial statements should factor in financial leverage in assessing reported earnings by lowering/upping their expectations as to the reliability of the earnings, depending on whether financial leverage is high or low.

Keywords: Real earnings management, Firm leverage, Accruals, Deferred tax

Financial Leverage on Earnings Management of Quoted Manufacturing Companies in Nigeria

1. Introduction

Many managers, accounting, and financial academics addressed the issue of earnings management over the past few decades. Schipper (1989) argues that earnings management is a deliberate management intrusion in the financial reporting process to gain personal benefits. Scott (2015) posited that earnings management accounting policies managers’ face that affects earnings. Healy and Wahlen (1999) assumed earnings control occurs when managers use judgment in economic reporting and in structuring transactions to adjust financial reviews to either deceive a few stakeholders, approximate the underlying company’s economic overall performance, or to steer final contractual results relying on reported accounting numbers. The profits management issue does not emerge in advanced nations exclusively (the Enron case, WorldCom case, Xerox case, and many others, including Nigeria has experienced some cases such as Cadbury Nigerian ltd 2007. The growing interest in the first-rate income renders the examination income control vital. It was previously addressed by Levitt. (2000). Additionally, studies on earnings management in emerging markets attracted researchers’ interest (Bao and Lewellyn., 2016).

Some studies focusing on these relationships still produce mixed results. Studies conducted by Defond and Jimbalvo (1994) and Chamberlain et al. (2014) found that leverage has a tremendous impact on profits management when agencies aim to reduce the violation of debt agreements and increase the businesses' bargaining value during debt negotiations. Beatty and Weber (2003), and Dichev and Skinner (2002) imply that a firm has excessive financial leverage due to the increase in accrual profits management and different income growing accounting decisions. This is due to avoiding debt covenant violations. Zagers (2009) found that in companies with increasing financial leverage, leverage causes income control with the purpose of influencing operational cash flow. Sari (2013) argues there’s a close connection between leverage and capital shape and expenditure. Debt is a settlement between a business enterprise acting as debtor and a creditor. The greater the leverage ratio, the higher the cost of the enterprise’s debt. Therefore, the corporation’s economic leverage can also initiate management to take earnings control. Some studies have found a negative connection between leverage and income control. Jelinek (2007) proposes that leverage will reduce earnings management. Zamri et al. (2013), Afza, and Rashid (2014), and Lazzem, and Jilani (2018) discovered that the level of leverage has the potential to reduce profits management. Companies with excessive leverage may face tighter manipulation from the creditor. Accordingly, management is less encouraged to engage in profits management.

Scholars like Ijiri (2013), advocated (with sound reasons) the need to maintain the reliability of reported earnings. On the other hand, notable accounting scholars such as Chambers (2005) advocated (with equally plausible logic) that earnings resulting from the accounting process should be relevant for the users’ decision making. Earnings management on the extreme was found to reduce the reliability of the reported earnings and, consequently, its relevance in users’ decision making (Bugshan, 2005). It is now a challenge for the present-day accounting scholars to find a way to improve earnings relevance while preserving its reliability- striking a balance without a tradeoff.

Capital market-based accounting researches (CMBAR) suggest that accounting earnings are value relevant if they show significant association with equity market (Barth, Beaver & Landsman, 2001, as cited in Bugshan, 2005). In 1968, Ball and Brown concluded that there is an association between accounting earnings and share returns (Easton & Harris, 1991). Following CMBAR studies, however, there is a lowering explanatory power of earnings on returns. While some researchers argued that error in methodology or the irrationality of the investors might be the cause of this weak relationship ( Lev, 2006), many researchers concluded with evidence, that the weak relationship between earnings and returns is the result of the low information content (low reliability) of the earnings that are being reported – due to the earnings management (Bugshan, 2005). Earnings management is reported to reduce earnings informativeness, misguided ill-equipped users and causes them to experience substantial losses. A typical example is the case of Enron’s earnings management, which eventually led to their downfall. In that case, it was revealed that the managers exploited the weaknesses in GAAP and continuously managed earnings using various techniques, like accrual earnings management, real earnings management, specific earnings management via deferred taxation and related party transactions, among others (Mehta & Srivastava are, 2009). The Nigerian case of Cadbury’s accounting irregularities and the lawsuit that followed in 2007 is believed to be the precedent in the country aiming to reduce corruption to attract foreign investment (Times Magazine, Suleiman T. 2007). The recent cases show some Nigerian banks, had their shareholders’ funds eroded without a trace, even though they have been reporting positively increased earnings (which is nonpermanent) through-out the periods. These cases were, along with other issues, believed to also be as a result of inadequate corporate monitoring (Eagle, 2009). These substantiate for the evidence that firms’ managers exploit the gaps embedded in GAAP to manage earnings. Studies documented that managers manage earnings using various strategies such as aggregate accruals (Healy, 1985), real transactions (Roychowdhury, 2006), and deferred tax expenses (Phillips pincus., 2002).

Studies have documented leverage impacts on accrual earnings management (Wasimullah, Toor& Abbas, 2010), as well as real earnings management (Mamedova, 2007). However, while some studies conclude that leverage constitutes a positive incentive to manipulate earnings using accruals and actual transactions (Mitani, 2010; Liu, 2011, respectively), others documented that leverage is a disincentive to the two earnings management strategies resulting in fault decision-making and consequently yielding ineffective outcome.

This paper consists of five (5) sections. Section one introduces a problem statement, and section two discusses the literature review. Section three discusses the methodology, and the fourth section focuses on the analysis and discussion of findings. The last section provides the conclusions.

2. Literature Review

2.1 Theoretical Framework

2.1.1 Positive Accounting Theory’s Debt/Equity Hypothesis

The study is based on the positive accounting theory’s debt/equity hypothesis, as propounded by Watts and Zimmerman (2008). Watts and Zimmerman (2013) posit the high-quality accounting concept, asserting that is connection between accounting numbers/variables, and that accounting pupils need to identify these styles prompting empirical evidence. Watts and Zimmerman (2013) identified a sample of positive connection between a firm’s leverage ratio and income-growing accounting choices. These is called debt/equity speculation or debt covenant speculation. As quoted in Sweeney’ (2004), “ceteris paribus, the larger a firm’s debt/fairness ratio, the more likely the company’s managers are to pick earnings-increasing accounting procedures”.

The higher the debt/equity ratio, the more firms are constrained within the debt covenants. The tighter the covenant constraint, the more the chances of a covenant violation and of incurring costs from technical default. While this is evident, the manager’s accommodate to exercise discretion by choosing earnings increasing accounting techniques to relax debt constraints and decrease the costs of technical default (John and Kalay, 2015).

The reason behind this, as Sweeney (2004) explained, is that accounting covenants are based primarily on the limit, and the handiest logical response is to conduct accounting manipulations. Expanding further, to safely protect funding in a given company, creditors impose specific regulations directly to the lending firm.

Those restrictions are formed as accounting ratios, expressing the minimum well known (of overall performance) required of the lender, i.e., the minimal cutting-edge ratio a firm must keep. The tightness of the ratios typically depends on the extent to which the firm relies on debt- i.e. leverage ratio. Similarly, the interest price, management fees, and tracking prices are typically factored inside the debt pricing. These are the borrowing fees.

Violating the covenants commonly leads to a refusal for lending renewal, finance shortage, renewal at higher borrowing fees, and liquidity trouble. Subsequently, the chain will cause bankruptcy wherein lenders will have the first claim. Therefore, violation of the debt settlement is expensive. To avoid from violation, Watts and Zimmerman (2013) suggest the rigid method through profits increasing accounting selections.

This predicts a positive relationship between leverage and earnings management.

2.1.2 Agency Theory

Agency theory posits that monitoring of an agent brings about reduced agency cost (Jensen and Meckling, 2013). The logic here is that earnings management is seen as agency cost since it is mostly opportunistic.

To avoid the agent’s dysfunctional behaviour, monitoring mechanism, such as debt monitoring conducted by lenders, comes in handy. The theory also argues (Jensen, 2013) that since debt requires servicing through interest plus capital instalment repayment, periodically, managers need to buckle up and generate more permanent earnings that will facilitate this (Jensen, 1986).

Thus, it is not rational to manage earnings where there is debt. As such, debt should have a negative impact on leverage.

2.3 Empirical Review

2.3.1 Leverage and Accrual Earnings Management

As stated in accounting literature, using the proponents of debt covenant hypothesis, managers of companies leading to the violation of debt agreements resort to manipulating accruals to avoid incurring the price attributed to the violation. Defond and Jiambalvo (2004) carried out a study on debt covenant violation and manipulation of accruals. They used a sample of 94 US corporations that had been known to have violated their debt covenants. In line with their speculations anticipating that managers’ accounting choices are motivated by the extent of closeness to debt agreement violation, the results imply there is a significant relationship between debt and strange accruals.

The result suggests in a year before the violation, strange, total and running capital accruals were significant, while during the 12 month violation period, the accruals are poor. They explain that the first result is based on the debt covenant speculating that firms manage earnings upwards to avoid violation.

The second result consisting of negative accruals shows that auditors undergoing subject qualification only after covenant violation, inspire the corporations to write off suspicious belongings. Typically only after a sturdy event like covenant violation with severe consequences the inspection is replaced.

According to the above explanation, everything fits. However, the studies covered most effectively firms which have already violated debt covenants. Examining firms that have not yet violated their debt covenant settlement may additionally provide a distinct result. Except for Jones’s (2001) time series and cross-sectional fashions used to proxy for peculiar accruals were severely criticised within the literature to be associated with gross estimation error.

For instance, Dechow et al. (2006) pointed out that it is erroneous for the Jones’ (2001) model to assume that the entire trade-in sales integrated within the version are non- discretionary. Each of Jones’s (2001) time collection and the move-sectional variations result in such an assumption. Similar research had been executed by Sweeney (2014) using the identical but larger population (one hundred thirty US Corporations) that violated debt agreements and got identical results. Defond and Jiambalvo (2004) found that managers with debt violation constraints respond with profit growing accounting alternatives. The difficulty here is that, in contrast to Defond and Jiambalvo, the study accounted for the time series of accounting changes of corporations near violation of debt agreements to proxy for income manipulation instead of regular accruals.

Considering the overall challenge of decreasing explanatory current of accounting earnings, Bugshan (2005) conducted a study on company governance, income management and the information content of accounting earnings. The study was conducted using a sample population of 778 of the top companies listed in Australian stock exchange, covering a period of 3 years (from 2007 to 2010).

Though his overall hypothesis proved to be correct- that corporate governance negatively impacts earnings management and conditioning corporate governance on earnings management (which reduces the informative earnings content) improves the informative earnings’ content. The author found leverage level, which is one of the monitoring mechanisms of corporate governance, has a positive impact on abnormal accruals.

This may be ascribed to the way he measured the leverage ratio. Welch (2011) severely criticised evidence and logic (refer to the discussion under section 2.4). Second, although correlation coefficient indicating a negative correlation between leverage level and abnormal accruals (-.13) is significant at 1%, the regression coefficient depicted a positive explanatory power of leverage at 0.16.

However, it is only the correlation result that is significant. Lastly, his study period is more than a decade old. With changes that occurred in the worlds’ economy, new researches may yield a different result. Evidence from the same Australian continent was presented by Jones and Sharma (2001), where they used a sample of listed firms over ten year period and found a positive relationship between leverage level and abnormal accruals.

Also, their result revealed that the earnings management detected from firms’ operations dating back to old regulation is far higher than after the provisions have been made extra stringent. They measured the leverage ratio because of the ratio of external debt to general legal responsibility. Considering leverage is taken into consideration to be the introduced pull-up on the agency’s equity, and total legal liability cannot stand for fairness or assets, their degree is arguably no longer acceptable leverage degree.

Further, they used the Jones (1991) version of discretionary accruals and the McNichols and Wilson (1988) model. While Jones’ model was criticised for having assumed that all changes in revenue are nondiscretionary, McNichols and Wilson (1988) model are considered inadequate as it captures only a single possible means of earnings management. Managers may employ several specific items at a time (Sun &Rath, 2010).

Nevertheless, using the same Taiwanese data obtained from 42 hospitals covering the period between 2005 to 2008, Huan and Liu (2011) examined the relationship between governance and earnings management. Their results were in line with findings of Shen and Chih (2007). Among the governance attributes, he measured leverage level, and it was defined as the ratio of long-term debt to total assets. His result shows a positive relationship between leverage (at scale) and abnormal accruals. In estimating the abnormal (discretionary) accruals, though he used the widely acclaimed model of discretionary accruals- the modified Jones (Dechow et al., 2005), instead of coefficients from the ordinary least square regression (OLS) to estimate the portion of managed earnings; he used the residuals from the regression to proxy for abnormal accruals. That may not affect the result, but using time series version is like assuming that the coefficients do not vary with time.

As Dechow et al. (2005) stated, the coefficients vary as time passes. Also, with the Coefficient computed separately for each year (using a cross-sectional approach), any firm in the industry can be used, and its earnings management for a given year can be ascertained (if the coefficients are meant to be industry-specific).

Thus, the work might not have provided potential other firms’ earnings management (in the industry but not included in his sample) to be ascertained. In addition, contrary to Welch (2011), this researcher assumed non-financial liabilities to be a non-debt item in computing the leverage ratio. Murhadi (2009) examined the relationship between good corporate governance practice and earnings management, using Indonesian listed firms, covering the period from 2014 to 2016. Among the organisational governance variables, he measured is leverage level using the Jones (2001) model to proxy for earnings management.

In support of agency theory, the outcome shows a negative relationship between leverage level and earnings management. However, the result is not significant. This could be due to employing Jones (2001) model, which is widely agreed to be measuring discretionary accruals with an error. Furthermore, he used the time series version. As Bugshan (2005) observed, time series version of Jones (2001) and modified Jones (Dechow et al., 2005) model assumes the coefficients to be static over time, whereas, they are time-specific. Thus, earnings management is better captured using the cross-sectional versions of the models. Also, three years’ observations for a time series might not be adequate (depending on the number of firms. No mention of the number of years was made in the paper).

Evidence from Japan by Mitani (2010), confirm the positive relationship between leverage and abnormal accruals. Mitani used cross-sectional Jones (2001) and Modified Jones (Dechow et al. (2005) models to estimate discretionary accruals. Results from both models are significant at 5% and 1%, respectively.

While he managed the shortcomings of using the time series version of the two models, he failed to consider the errors in Jones (2001). He modified Jones (Dechow et al., 2005) by assuming that all change in revenues is nondiscretionary, and all change in receivables are discretionary. Perhaps employing the Dechow et al., (2002) forward-looking model, which Zhang (2002) adopted and found to be robust and devoid of these shortcomings, might yield a different result. Although all the results (that are significant) discussed so far are in support of debt covenant hypothesis- presuming leverage to be positively related to abnormal accruals, Sercu et al., (2006) argued that the explanation for this positive relation is much subtler than the proponents of debt covenant hypothesis suggested.

They noted that the explanation that managers resort to managing earnings to avoid the cost of debt covenant violation is merely inadequate. How can the debt covenant hypothesis otherwise explain the positive relationship between debt and companies’ earnings management whose debts have no covenants? They cited the example of some Belgian firms whose creditors helped them recovered from potential distress since they had stakes to lose if the firms would undergo problems. They thus suggested that other broadens the costs of financial distress, could be a better explanation for this relationship.

If this is presumed to be accurate, then it could be said that managers manage income increasing accruals upward not just to comfort the lenders but also to assure other stakeholders like shareholders, trade creditors, who do not impose any covenant but have more to lose than the organised lenders (who are covered by insurance) in the event of financial distress. Sercu et al. (2006) conducted research using Belgian non-listed firms (where debt covenants hardly exist), to find the impact of leverage and earnings management. In their work, they measured leverage increases and leverage levels using bank loans and then trade creditors, separately. After regressing each measure against the empirical proxy of earnings management (abnormal accruals), they discovered that both measures of earnings management show a significant positive relationship with earnings management. They concluded that the cost of debt covenant violation should not be used to explain the leverage level, leverage increases, and earnings management’s positive relationship and that the cost of financial distress explains it better. Diamond (1991) posited that the presence of debt, especially bank debt or bonds in a firm should signal reassurance to the potentially worried stakeholders (such as suppliers, and potential investors) since it signifies lenders confidence in the firm, who may seem better informed, given the information asymmetry; is contradicted.

If this debt signalling quality is to be considered, then the need for earnings management to reassure these stakeholders would not arise, as it would be taken care of by the debt presence. Thus, a negative relationship should have depicted when leverage is measured by trade creditors. Surveying population and data differing from this European country may conform with Diamond (2001).

Contrary to the above findings, evidence from Pakistan documented by Wasimullah et al. (2010), shows a significantly negative association between high leverage, leverage increases leverage level and total and abnormal accruals. They used a sample of 182 textile firms listed in Karachi Stock Exchange for the period 2010-2016 and concluded that high leverage is indeed instrumental in controlling the opportunistic behaviour of managers.

Though the result is robust for three different measures of abnormal accruals (the Healy, 2005), modified Jones (2005) and the forward-looking model of Dechow et al., (2002), they used a dummy variable to proxy for leverage, they partitioned their sample between firms that undergo leverage increase in a given year as 1 and 0 if otherwise, in the first test.

In the second test, they partitioned the samples between highly leveraged firms as 1 and 0 if otherwise. In all the tests, they found a significant negative association between leverage and abnormal accruals. Without controlling for the leverage increases, the question here is what if the result obtained is as a result of the interacting effects of the three explanatory variables (i.e. leverage increases, high leverage, and leverage level)? What would be the result if the only a raw figure of the leverage ratio is used?

2.3.2. Leverage and Real Earnings Management

Most earnings management researches focus on accrual earnings management, leaving other avenues unexplored. Mamedova (2007) provides evidence that as a result of corporate scandals in the last two decades, investors, creditors, and shareholders seem to have lost faith in “soft numbers” (reported earnings). Instead, they are now after the “hard numbers” (cash flow).

Due to the shift in yardstick for assessing performance, Zang (2006) provided empirical evidence that managers would rather manage earnings through real action than accrual action. This is in line with the result of Graham et al., (2005), where it is reported that firm managers would go to the extra-mile of decreasing discretionary spending, as well as delaying the take-off of new projects to meet earnings targets, even if such delay would result with value decrease.

This suggests that to maintain accounting appearance, managers are ready to take real economic actions. Managers are prepared to burn tangible financial assets, compromise optimal economic alternatives for the sake of reporting attractive accounting “hard numbers” to impress the users.

There seems to be a constant tension between a firm’s short-term and long-term objectives, which is detrimental to the firm’s overall goal (Mamedova, 2007). Mamedova (2007) observed that in the era of a globalising economy, these are generally funded through equity fund and external financing. With an increased demand for loans and high interest, firms are required to continually generate sufficient cash flows to meet requirements from lenders or else risk bankruptcy or a takeover.

For this reason, she added, yeasty-minded managers would resort to real earnings management that could generate more cash flow to receive or maintain external finances. Consequently, she noted, leverage level and leverage increase should have a positive impact on real earnings management. Conversely, according to Jensen’s (2006) control hypothesis, leverage controls the opportunistic behaviour of managers and in that; high leverage begets more demand on the firm’s cash flow.

Since a considerable amount of a firm’s free cash flow is channelled to debt servicing, managers are left with little cash. When this happens, rationally, they do not engage in unproductive activities, but instead, channel the available cash into more prudent uses. Consequently, this hypothesis predicts that leverage should be negatively related to real earnings management.

Contrary to the above prediction, the result of Kim, Lei, and Pevzner (2010) depicts a positive relationship between real earnings management and leverage. Their evidence indicates that tightness of debt covenant is positively related to real earnings management, and this finding stands for both the period before and after the Sarbanes Oxley Act.

They measured leverage as the ratio of a firm’s total liability to total assets, which is quite acceptable to this research, considering Welch’s (2011). However, they used data from US-listed firms as Kim et al. (2010), using the same US data. This resulted in the same mixed results obtained by Mamedova (2007). Findings indicate that by distinguishing between highly leveraged firms and firms that underwent leverage increases, debt induces firms to manipulate activities through real actions when an absolute value of debt is used in place of leverage.

When the debt-to-equity ratio of book value is used, the results show a negative relationship to no significant probability. Where the debt-to-equity ratio computed using market value is adopted, the result shows a positive but non-significant relationship between high leverage, leverage increases and real earnings management. Real earnings management were measured using the normal cash flow model, as implemented by Roychowdhury (2006).

Leverage ratios were measured using the ratio of debt to equity plus debt (the book, and market values). However, she also used the absolute value of debt to proxy for leverage, and this measure is the only proxy with a significant result. In line with the criticisms on measures of leverage stated earlier, this research does not rely solely on the absolute value of debt as leverage measure. Different measure (like a total liability to the total assets) and diverse populations may yield a different result. Jensen’s (2006) agency cost of free cash flow relates to finding a practical way of using up free cash flow to avoid the agency cost associated with it.

As the theory posits, the agency cost of free cash flow stems from the separation of ownership and management. Opportunistic managers may be driven by the available free cash flow to expand the firms beyond its optimal size, with the aim to expand their power and compensation (Jensen, 2006). Jensen (2006) noted that one of the ways to use up the free cash flow judiciously is through dividend payment, and thus, managers will be forced to seek more external financing, which will subject them to financers’ scrutiny.

Liu (2011) researched the impact of dividend policy and real earnings management, as well as relationships with real earnings management. Following Roychowdhury (2006), he measured real earnings management using an abnormal cash flow model, and other real earnings management models.

His results indicate that the higher a firm’s leverage, the higher its abnormal cash flow. This supports the debt covenant hypothesis and contradicts the free cash flow hypothesis of Jensen (2006). According to Jensen (2006), excess cash flow is supposed to be used up in debt servicing (along with the dividend payments mentioned above), meaning, the more of debt begets, the higher the demand on the abnormal cash flow. Though the work of Liu (2011) is recent, the data used is from a developed economy (US).

As cited in Herman, Inoue and Thomas (2001), Shippers (1989) observed that a specific proxy for earnings management needs not to be discretionary all the time, but significant enough to matter. Considering that real earnings management may take the form of asset sales, Herman, et al., (2001) examined the impact of asset sales on earnings forecast using Japanese listed firms.Having observed the predicted effect of leverage incentive on earnings management, they controlled for leverage ratio. They measured it as the ratio of long term liability to total assets. Their result shows that managers in Japanese listed firms employ assets sales in years when earnings are below the prior year’s forecast. They also discovered that the leverage ratio has a positive impact on the proceedings from assets sales. This finding is no different from all (but Mamedova, 2007) the previous findings on the effects of the leverage on real earnings management. Nevertheless, the use of asset sales to proxy for real earnings management excludes other possible real discretionary actions that may have an incremental impact on cash flow.

Hanlon and Rochester (2009) explored leverage and deferred tax expenses. Tax research is multi-disciplinary and most accounting researchers shy away from it. This may be the reason why there is scanty literature exploring the use of deferred tax in manipulating earnings, compared to the researches on the use of other techniques like abnormal accruals. Several studies on deferred tax and earning management are now gradually developing in different forms. Due to the multi-disciplinary nature of tax research, replication is problematic. Tax laws vary among countries. For instance, some investigations on deferred tax and earnings management in the US investigate the use of under/over the provision of a deferred tax valuation allowance to manage earnings.

The international accounting standards (IAS12) allow for partial provision. However, there is no single home-based research on the use of deferred taxation to manage earnings, even though some other dimensions can still be carried out in Nigeria without grappling with these differences. One such is the use of Net change in deferred tax liability (i.e. net deferred tax expense) to manage earnings. One may expect to find a discussion relating to documented evidence on the relationship that exists between deferred tax earnings management and leverage incentive.

We should take a note that there is no known empirical evidence (to the best of our knowledge) as to the nature of this relationship. Nevertheless, evidence exists as to the monitoring/inducing power of leverage to avoid/engage in earnings management. Also, little evidence exists on the strength of deferred tax expenses in managing earnings. This is discussed below. After the discussion, a nexus between deferred tax earnings management and leverage incentive should be evident. Phillips et al. (2002) proposed that deferred tax expense is efficient in detecting earnings management since managers typically have more discretion under GAAP than under tax rules.

If managers are to manage earnings upwards, they are expected to exploit their discretion under GAAP in ways that are not disruptive to current taxable income. The accounting choices they make will generate differences between the accounting income reported and taxable income, that increases deferred tax expense. Phillips et al. (2002) investigate the practice of earnings management to avoid reporting loss and to avoid a decline in earnings. He used three different proxies of earnings management- deferred tax expense, total and abnormal accruals. He concluded that among the three metrics of earnings management, deferred tax expense is more useful than other measures and that deferred tax expense is significantly more accurate than any of the accrual metrics in classifying firms as successfully avoiding loss. Following Phillips et al., (2002), Zhang (2002) used deferred tax expense (net change in deferred tax liability), scaled by lagged total assets, as a proxy for earnings management to report evidence of earnings management in rounding up earnings per share (EPS) figure. In his research, he used nine different metrics of earnings management- eight accrual models, and the deferred tax expense. The result shows that deferred tax expense detects more discretion of managers in managing earnings. Deferred tax expenses allowed for the detection of the type of earnings management associated with rounding up earnings per share, while accrual models did not.

Because earnings management, by definition, is represented in accruals, the obvious question will be: why is deferred tax expense better than discretionary accruals in this case? To answer this question, Zhang conducted robust checks on some of the items identified as a source of deferred tax expenses. He zeroed on depreciation expenses, bad debt expenses and prepaid expenses (because they are readily obtainable from financial reports).

He observed that lousy debt expenses reduce accounting (book) income, but not tax income. This is because methods for tax write-offs are restricted to specific account failures, instead of the estimates of the expected account failures allowed under GAAP. As such, they are reducing lousy debt expenses, increasing book income and also deferred tax expenses. Since bad debt expenses are not directly depicted, Zhang (2002) used the ratio of allowance for doubtful debt divided by total account receivable.

He assumed that any change in this ratio is earnings management. He used total depreciation expenses divided by total assets. Upward or downward differences in ratio and change in the applied method for charging depreciation prompted a change in book income and deferred tax expense. Reducing depreciation expenses increases book income and deferred tax expenses Zhang (2002) observed.

To gauge the effect of prepaid expenses, he used prepaid expenses divided by total assets. GAAP requires prepaid expenses to be written off over the periods when benefits are received, while tax laws require it to be written off in the payment year. Zhang observed that this brings about book/tax income differences. Correlating the three items with deferred tax showed a strong positive correlation. Regressing them with the proxy for earnings management incentive, Zhang noticed that these items are the source of earnings management, with lousy debt being the strongest. He concluded that deferred tax expenses detected earnings management in his research more significantly than abnormal accrual models because abnormal accrual models (forward-looking model inclusive) do not capture the specific source of accruals, such as bad debt expenses, whereas deferred tax expenses do capture them.

Additional evidence from South Africa was documented by Rabin and Nagesh (2006). They examined the practice of earnings management to avoid losses or earnings decline. With regards to their observation on Phillips et al., (2002), they noted that when deferred tax expense is used as a surrogate for earnings management, the errors associated with isolating discretionary accruals are avoided. Along with accrual models, they used deferred tax expense to represent the discretion of the managers. The result indicated that total accrual is incrementally more useful than deferred tax expense in detecting managing earnings to avoid reporting decline in earnings. Deferred tax expense is progressively valuable beyond total accrual in detecting managing earnings to avoid loss.

Dhalilwal et al. (2004) examined the technique used by managers to manage earnings (to avoid the loss or beat analyst forecast) as a last resort, just before the earnings announcement. They concluded that with regards to the complexity of estimating tax expense and the timing of the tax accrual before earnings announcements, tax expense is a significant and under-explored context in the study of earnings management. When managers have an incentive to achieve a particular earnings target, the tax expense account provides a final opportunity for earnings management.

Tax expense is one of the last accounts closed before earnings are announced because other income-related changes affect the tax account. We consider tax expense because it is meaningful for many firms and because it contains the necessary discretion to generate information asymmetry between managers and investors or analysts. It is interesting to note that though Dhalilwal et al., (2004) did not use deferred tax expense directly, the tax expense account they used comprises of tax paid for the current year and tax-deferred to a future date. Thus, the usefulness of deferred tax expense is still reflected in their research. Many other inquiries exist on the use of under/over provision for deferred tax valuation allowance to manage earnings, but as stated earlier, Nigerian tax regulations make it impossible to manage earning using this technique. Hence this research finds it best not to discuss them.

Considering the startling efficacy of deferred tax expenses as an earnings management tool; and referring to the prediction of positive accounting theory – the higher the debt to equity ratio, the more potentials for managers to employ income increasing accounting choices. Suffices to say, deferred tax expenses emanating from income increasing accounting choices (as argued by the findings above) will be positively related to leverage. One may argue that the negative/positive relationship between debt/equity financing and income tax payable (tax effects of leverage financing) may bias the result of matching leverage against deferred tax expense. Scrutiny of these subtle relationships reveals that deferred tax expenses emanate from manipulation that does not interfere with taxable income and the tax payable for the period.

Philips et al. (2003) noted that deferred tax expenses consist of only temporary differences emanating from non-debt tax shields, like depreciation expenses, bad debt expenses, research and development, etc. As such, the relationship between leverage ratio and deferred tax expenses is not affected by the relationship that exists between leverage ratio and income taxpayers.

In light of these mixed results and controversies, this study seeks to address the extent to which financial leverage influence the opportunity and tendency of managers to manage earnings using accruals. We aim to find out the actual direction of the impact of leverage on real earnings management. Our objective is to explore how leverage impacts the use of temporary difference (deferred tax expense) to manage earnings in Nigeria.

3. Methodology

The quasi-experimental (survey) research design was adopted because various elements of the model are not under the researcher’s control. The cross-sectional survey method was adopted in this study. As the secondary source, researchers gathered data by examining the existing documents.

This method enabled us to collect data for all the variables in the study from the Nigerian Stock Exchange (NSE) factbook and published annual reports. The study population consisted of 79 all quoted manufacturing companies in Nigeria as of December 2016. Within this sampling procedures, 29 quoted manufacturing companies were considered because they submitted their audited reports at a stipulated deadline on December 31, 2016, which therefore enabled the researcher to pick data.

Model Specification

This model will be built and modifies in line with hypothesis formulated in this study, AEM = f(LEV) (1)

REM = f(LEV) (2)

DTEM = f(LEV)

(3) The econometric specification of the explicit form of the regression models are given as follows;

AEM = a0 + a1LEV + e (4)

REM = b0 + b1LEV + e (5)

DTEM = d0 + d1LEV + e (6)

Where,

AEM = Accruals Earnings Management

REM = Real Earnings Management

DTEM = Deferred Tax Earnings Management

LEV = Leverage

a0, a1, b0, b1, d0, and d1 are coefficients of the explanatory variables,.e = error term A priori Expectation: a0> 0, a1>0,b0> 0, b1> 0, d0> 0, d1>0

4. Analysis and Discussion of Findings

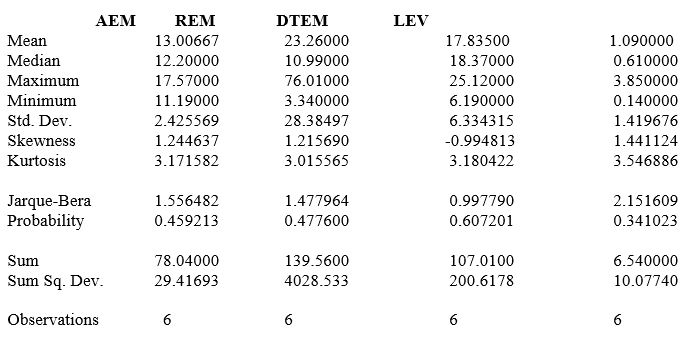

4.1 Descriptive Statistics

Table 4.1 above shows that leverage has a mean value of 1.1 with an associated standard deviation of 1.4, while accruals earnings management has a mean value of 13.00 with an associated standard deviation 0f 2.42. Furthermore, real earnings management and deferred tax earnings management have a mean value of 23.26 and 17.83 with associated standard deviations of 28.38 and 6.33, respectively.

This implies that leverage has more influence on real earnings management than accruals earnings management and deferred tax earnings management, respectively, with a higher level of risk intake in the process for the period under study.

4.2 Regression Results

Table 4.2.1: Regression Results First Model

Source: Author’s computation: E-view 9

Source: Author’s computation: E-view 9

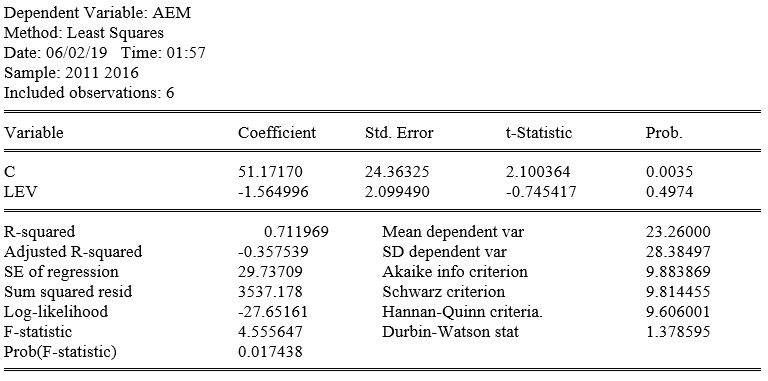

Table 4.2.1 examines the impact of leverage on accruals earnings management in the listed manufacturing companies in Nigeria. This means that leverage has no significant impact on accrual earnings management in listed firms for the period under study. Therefore, the null hypothesis is accepted and we conclude that leverage level has no significant impact on accrual earnings management in listed manufacturing firms in Nigeria for the period under study.

Furthermore, the results of the test of the overall significance of the model using F-statistics shows that the entire model is statistically significant. We arrive at this conclusion because the F-statistics of 4.555647 is greater than the F-probability of 0.017438. The coefficient of determination (R2) indicates that the predictor variable explains 71 % of total variation of accruals earnings management (AEM) in the model (LEV). This means that the model is a good fit.

Finally, the Durbin-Watson statistics, a rule of thumb for the measure of autocorrelation is greater than the R2 (1.378595>0.711969) thus, indicating the absence of the first-order autocorrelation.

Table 4.2.2: Regression Results Second Model

Source: Author’s computation: E-view 9

Source: Author’s computation: E-view 9

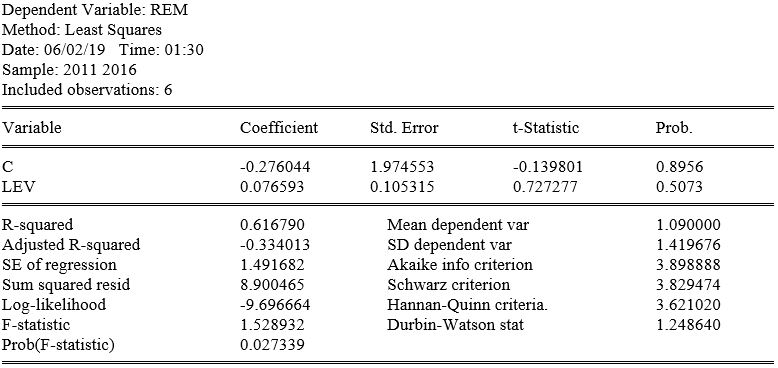

Table 4.2.2 above revealed that leverage (LEV) has a t-statistic of 0.727277 with an associated probability value of 0.5073, which is greater than 5% level of significance. This means that leverage has no significant impact on real earnings management in listed manufacturing firms in Nigeria for the period under study.

Therefore, the null hypothesis is accepted and we conclude that leverage level has no significant impact on real earnings management in listed manufacturing firms in Nigeria for the period under study.

Furthermore, the results of the test of the overall significance of the model using F-statistics shows that the entire model is statistically significant. We arrive at this conclusion because of the F-statistics of 1.528932is greater than the F-probability of 0.027339. The Coefficient of determination (R2) of the model indicates that approximately 62% of the total variation of real earnings management (REM) is explained by the leverage (LEV). This means that the model is a good fit.

Finally, the Durbin-Watson statistics, a rule of thumb for the measure of autocorrelation is greater than the Coefficient of determination (R2) (1.248640>0.616790) thus, indicating the absence of the first-order autocorrelation.

Table 4.2.3: Regression Results Third Model

Source: Author’s computation: E-view 9

Source: Author’s computation: E-view 9

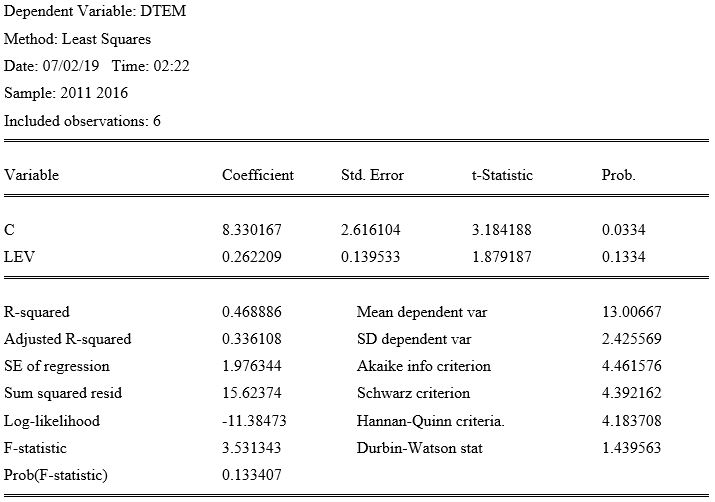

Table 4.2.3 revealed that leverage (LEV) has a t-statistic of 1.879187 with an associated probability value of 0.1334, which is greater than 5% level of significance.

This means that leverage has no significant impact on deferred tax earnings management in listed manufacturing firms in Nigeria for the period under study. Therefore, the null hypothesis is accepted and we conclude that leverage level has no significant impact on deferred tax earnings management in listed manufacturing firms in Nigeria.

The results also show that leverage (LEV) is linear (positive) and statistically insignificant to deferred tax earnings management (DTEM). Furthermore, the results of the test of the overall significance of the model using F-statistics shows that the entire model is statistically significant. We arrive at this conclusion because the F-statistics of 3.531343 is greater than the F-probability of 0.133407.

The Coefficient of determination (R2) of the model indicates that approximately 47% of the total variation of deferred tax earnings management (DTEM) is explained by the leverage (LEV). This means that the model is not a good fit. Finally, the Durbin-Watson statistics, a rule of thumb for the measure of autocorrelation is greater than the Coefficient of determination (R2) (1.439563>0.468886) thus, indicating the absence of the first-order autocorrelation.

4.3 Discussions of Findings

The results of the analysis of this study reveal that the management of listed manufacturing companies in Nigeria employs all the three methods of earnings management (namely, accrual earnings management, real earnings management, and deferred tax earnings management). This is in line with the work of Sun and Rath (2010), whose results indicate that firms are likely to employ more than one technique in managing earnings simultaneously.

The analyses further revealed that the relationship between the explanatory variable (leverage) and each of the dependent variables (accruals earnings management, real earnings management and deferred tax earnings management) varies. That is, leverage has a nonlinear (negative) relationship with accruals earnings management, while that of real earnings management and deferred tax earnings management depict a linear (positive) relationship with leverage. This indicates that leverage does have a bearing on earnings management with variability.

The results also reveal that leverage level does not have a significant impact on accruals earnings management in listed manufacturing firms in Nigeria. The same applies to real earnings management and deferred tax earnings management, respectively. The implication is that leverage level has no significant impact on the management of earnings in listed manufacturing firms in Nigeria for the period under study.

The findings in this study are contrary to the notion of Watts and Zimmerman, (2013), which upholds that the higher a firm’s debt to equity ratio, the more likely that managers manage earnings. It, however, conforms to the work of Jensen and Mecklings (2013) that leverage controls for managers’ opportunistic tendencies.

The explanation of superiority financial leverage has over total leverage, non-impact on accrual earnings management as well as real and deferred tax earnings management lies in very contradicting wordings of the positive accounting’s debt covenant hypothesis. The hypothesis correctly used the term debt-to-equity ratio, and that is exactly the measure of financial leverage.

It is unlike total leverage as total leverage includes non-financial liability in the numerator, and the denominator comprises of total assets. The debt covenant hypothesis clarifies that high debt-to-equity induces managers to employ income increasing accounting choices, to avoid incurring the cost of violating the agreements made with the lenders.

It is therefore pertinent to note here that accounting choices do not typically associate with accruals and the other earnings management measures employed in the study. The findings also contradict the work of Mamedova (2007) and the prediction of agency theory. However, they are in line with the work of Kim et al. (2010) and the prediction of the debt covenant hypothesis.

Thus, the explanation here for the negative relationship is that, the more a firm is indebted, the less likely it will engage its necessary resources into sub-optimal undertaking producing abnormal cash-flow. The cogency here is that debt owners are monitoring the managers’ choice of projects/investments to ensure that they engage in cash-generating activities that are viable and economically optimal. This applies not just on a short-term basis but also in long-term since debt is of a long-term perspective.

They do this to secure the safe return of their investment (principal) and the return on their investment (interest), from the firm. On the other hand, the presence of debt in a firm consumes any free-cash-flow, inducing managers to engage in ventures that are not economically beneficial to the firm as much as it is for a manager.

Meaning, debt curbs the problem associated with free-cash-flow (agency cost of free-cash-flow), as the excess cash is being used up in debt servicing, settlements or repayment. The finding also justified the notion forwarded by Welch (2011) that not only financial debt should be considered as debt. Non-financial debt equally has a claim on a firm’s assets in the day to day operations and in the event of liquidation, their settlement also consumes cash-flow.

5. Conclusion, Implication and Recommendations

The study investigated financial leverage on earnings management of manufacturing firms in Nigeria. From the analytical output, the study concluded that debt-covenant hypotheses best suits accounting-based earnings management and financial leverage; as financial liability is the sort of debt that comes along with covenants/agreements. The inference derivable here is that firms manage earnings upward, to thwart the cost of violating debt agreements.

However, financial and total leverage have notable negative impacts on real earnings management. This is logical in the sense that, just like fiscal liabilities, non-financial liabilities too put pressure on a firm’s cash-flow. Thus, the more the leverages (the responsibilities), the more the pressures, and consequently, the less excess (abnormal) cash will remain to be reported.

Therefore, earnings management on leverage has notable negative impacts on deferred tax earnings management. Obtaining the same pattern here can be justified by the interwoven affiliations existing between depreciation and deferred tax in one hand, and depreciation and cash-flow in the other side. Note that depreciation is part of the cash-flows’ non-cash items- due to its tax/cash saving trait.

The study recommends Government and other regulatory authorities should implement workable and effective policies to motivate further and encourage managers to enhance accruals earnings management strategies to gain more confidence from both domestic and allied investors in the manufacturing sector.

Leverage of listed manufacturing firms in Nigeria suggests board members should redesign management strategies to reach objectives, improve real earnings management strategies, and restore the confidence of regulatory authorities in the manufacturing sector. This may be accomplished by ensuring transparency and open declaration of profit before tax values to avoid annual financial window dressing of balance sheets by companies in Nigeria. This proceeding recommendation is based on the fact that Government should ensure peace and stability in the socio-economy and political system of the nation by stopping religion and ethnic crisis and encourage more foreign investors into the manufacturing sector.

References

- Afza, T., and Rashid, B. (2014). Opportunistic earnings management, debt, and diversification: Empirical Evidence for Manufacturing Firms of Pakistan. Sci. Int. 26 (5), 2489–2494.

- Bao, S. R., and Lewellyn, K, B. (2016). Ownership structure and earnings Management in Emerging Markets: An Institutionalised Agency Perspective. International Business Review. Vol. xxx. Page. Xxxxxx.

- Beatty, A., and Weber, J. (2008). The effects of debt contracting on voluntary accounting method The Accounting Review, 78 (1), 119-142. Crossref

- Barth, M., Beaver, W. and Landsman, W. (2001). The relevance of the value relevance literature for financial accounting standard setting: another view. Journal of Accounting and Economics, 31, 1-3. Crossref

- Beatty, A., Chamberlains, S. and Magliolo, J. (1995). Managing financial report of commercial banks: The influence of taxes, regulatory capital, and earnings”. Journal of Accounting and Economics, 22, 207-240.

- Bugshan, T. (2005). Corporate governance, earnings management, and the information content of accounting earnings: Theoretical model and empirical tests. Unpublished Ph.D Thesis, Bond University Queensland 4229, Australia.

- Capital Gains Tax ACT. (1967). Law of the Federation of Nigeria. ACT No. 44, Amended version of 1999, ACT No. 45.

- Chambers, R. J. (2005). Accounting evaluation and economic behavior. Englewood Cliffs, Inc. New Jersey, Prentice-Hall.

- Companies Income Tax ACT CAP 60 LFN (1990) ACT 2004 Amendments.

- Dechow, P. and Sloan, R. (1991). Executive incentives and the horizon problem: An empirical investigation. Journal of Accounting and Economics, 14, 51-89. Crossref

- Dechow, P. and Skinner, D. (2000). Earnings management: reconciling the views of accounting academics, practitioners, and regulators. SSRN Working paper. Crossref

- Dechow, P., Sloan, R. and Sweeney, A. (1995). Detecting earnings management”. The Accounting Review, 70 (2), 193-225.

- Dechow, P.M., Richardson, S.A. and Tuna, I. A. (2002). Are small profit firms boosting accruals to avoid losses and are they different from small loss firms?. Working paper, University of Michigan.

- DeFond, M. and Jiambalvo, J. (1994). Debt covenant violation and manipulation of accruals. Journal of Accounting and Economics, 17, 145-176. Crossref

- Defond, M. L. and Jiambalvo, J. (1991). Incidence and circumstances of accounting errors”. The Accounting Review, 66 (3), 643-655.

- Degeorge, F., Patel, J. and Zeckhauser, R. (1999). Earnings management to exceed thresholds. Journal of Business, 72. Crossref

- Dhaliwal, D. C., Gleason, and Mills, L. (2004). Last chance earnings management: Using the tax expense to achieve earnings targets. Contemporary Accounting Research, 21(2), 431-458. Crossref

- Diamond, D. W. (1991). “Debt maturity structure and liquidity risk. The Quarterly Journal of Economics, 106 (3), 709-737. Crossref

- Dichev, I. D. and Skinner, D. J. (2001). Large-sample evidence on the debt covenant hypothesis. Journal of Accounting Research, 40 (4), 1091-1123. Crossref

- Dictionary of Financial and Business Terms, (2007). Retrieved from http://www.wiziq.com/tutorial/23752Dictionary-of-Financial-and-Business-Terms-pdf, accessed: 21th August 2011.

- Hanlon, M. and Heitzman, S. (2010). A review of tax research”. University of North Carolina Tax Symposium, Conference Paper. Crossref

- Healy, P. and Wahlen, J. (1999). A review of the earnings management literature and its implications for standard setting. Accounting Horizons, 13 (4), 365-384. Crossref

- Healy, P. (1985). The impact of bonus schemes on the selection of accounting principles. Journal of Accounting and Economics, 85-107. Crossref

- Herman, D., Inoue, T. and Thomas, W. B. (2001). The sale of assets to manage earnings in Japan”. University of Oklahoma, workshop Paper. Crossref

- Huang, D. T. and Liu, Z. C. (2011). The relationships among governance and earnings management: An Empirical study on non-profit hospitals in Taiwan”. African Journal of Business Management, 5 (14), 5468-5476.

- Ijiri, Y. and Jaedicke, R. K. (2013). Reliability and objectivity of accounting measurement. The Accounting Review, 41(3), 474-483.

- Jensen, M. and Meckling, W. (2013). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3005-360.

- Jensen, M. (1986). “Agency costs of free cash flow, corporate finance, and takeovers”. American Economic Review, 76, 323-329.

- John, E. I. (2008). SAS Accounting Standards for Exams. Lagos, Accounting Training and Publication.

- John, K. and Kalay, A. (1982). Costly contracting and optimal payout constraints. Journal of Finance, 37 (2), 457-470. Crossref

- Jones, J. (1991). Earnings management during import relief investigations”. Journal of Accounting Research, 29 (2), 193-223. Crossref

- Jones, S. and Sharma, R. (2001). The impact of free-cash flow, financial leverage and accounting regulation on earnings management in Australia’s old and new economies. Journal of Managerial Finance, 27 (12), 18. Crossref

- Kim, Y., Liu, C., and Rhee, S. G. (2003). The relation of earnings management to firm size. Social Science Research Network.

- Kim, B. H., Lie, L. and Pervnezer, M (2010). Debt covenant slack and real earnings management”. Working Paper, American University Kogod School of Business and George Mason University School of Management, M40/M41.

- Lazzem, S., and Jilani, F. (2018). The impact of leverage on accrual-based earnings management. The case of listed French firms. Research in International Business and Finance, 44: 350-358.

- Levitt, A. (2000). Testimony concerning commission’s auditor independence proposal before the senate subcommittee on securities committee on banking, housing, and urban affairs, September 28. http://www.sec.gov/news/ testimony/ts152000.html.

- Lee, Y. W., Yu, T. and Zhang, T. (2007). Do corporations manipulate earnings to meet or beat analysts’ forecasts? evidence from pension plan assumption changes. Working Paper, University of Rhode Island, Kingston, RI/02881.

- Leuz, C., Nanda, D. and Wysocki, P.D. (2003). Investor protection and earnings management: An international comparison”. Journal of Financial Economics, 69, 505–527. Crossref

- Lev, B. and Kunitzky, (1974). On the association between smoothing measures and the risk of common stocks. The Accounting Review, 70(2), 259-270.

- Levitt, A. (1998). The ‘numbers game’”. nyu center for law and business, New York, Centre for Law and Business, New York, The CPA Journal, 14.

- Liu, N. (2011). The role of dividend policy in real earnings management. Georgia State University Digital Archive, Working Paper.

- Mamedova, Z. I. (2008). The effects of leverage increases on real earnings management”. Erasmus university, Netherland, Working paper.

- Mitani, H. (2010). Additional evidence on earnings management and corporate governance. Financial Research and Training Centre, Discussion paper, DP2009-7.

- Modigliani, F. and Miller, M. (1958). The cost of capital, corporation finance, and the theory of investment. American Economic Review, 46, 261–297.

- Modigliani, F. and Miller, M. (1963). Corporation income taxes and the cost of capital: A correction. American Economic Review, 53, 433–443.

- Murhadi, W. R. (2009). Good corporate governance and earnings management practice: An Indonesian Case”. Munich Personal RePEc Archive (MPRA) Paper. Crossref

- National Association of Certified Fraud Examiners (1993). Cooking the book: What every Accountant should know about Fraud, Self-study Work-book. No.12, 92-5401

- Phillips, J., Pincus, M. and Rego, S. O. (2002). Earnings management: New evidence based on deferred tax expenses. University of Connecticut, Working Paper. Subsequent version: (2003), Accounting Review, 78(2), 491-521. Crossref

- Phillips, J., Pincus, M., Rego, S. O. and Wan, H. (2003). Decomposing changes in deferred tax assets and deferred tax liabilities to isolated earnings management activities. University of Connecticut and University of Iowa, Working Paper. Crossref

- Rabin, E. and Nagesh, M. (2008). Earnings management and deferred taxes, preliminary evidence from South Africa”. School of Accountancy, University of Witwatersrand, Johannesburg, Working paper.

- Roychowdhury, S. (2006). Earnings management through real activities manipulation. Journal of Accounting and Economics, 42(3), 335-370. Crossref

- Schipper, K. (1989). Commentary on earnings management. Accounting Horizons, 3 (4), 91.

- Sari, S. R. (2013). Pengaruh Leverage Dan Mekanisme Good Corporate Governance Terhadap Manajemen Laba. Jurnal Ilmu and Riset Akuntansi, 2(6). Crossref

- Scott, W. (2015). Financial Accounting Theory. Second Edition. Scarborough, Ontario: Prentice Hall Canada Inc.

- Scott, J. H. (1976). A theory of optimal capital structure. Bell Journal of Economics, 7, 33-54. Crossref

- Sercu, P.; Bauwhede, V. H. and Willekens, M. (2006). Earnings management and debt. International Symposium on Auditing Research, Sydney.

- Skinner, D. J. and Sloan, R.G (2002). Earnings surprises, growth expectations, and stock returns or don’t let an earnings torpedo sink your portfolio. Review of Accounting Studies, 7(23), 289-312.

- Suleiman, T. (2007). Cadbury Nigeria sued by investors over accounting. The Sunday Times.

- Sun, L. and Rath, S. (2010). Earnings management research: A Review of contemporary Research Methods”. Global Review of Accounting & Finance, 1, 121-135.

- Sun, W. and Sun, J. (2007). Analysis of factors influencing manager’s Earnings management intention”. Working Paper, Agricultural University, Hebei, PR China,

- Sweeney, A. (2004) “Debt-Covenant Violations and Managers’ Accounting Responses”. Journal of Accounting and Economics, 281-308. Crossref

- Vakilifard, H., and Mortazari, M. S., (2016). The impact of financial leverage on accrual-based and real earnings management. International Journal Academic Researching Accounting Financial Management Science, 6(2): Crossref

- Wang, Z. and Williams, T. H. (1994). Accounting income smoothing and stockholder wealth”. Journal of Applied Business Research, 10(3), 96-104. Crossref

- Wasimullah, Toor, U.I. and Abbas, Z. (2010). Can high leverage control the opportunistic behavior of managers: Case analysis of textile sector of Pakistan”. International Research Journal of Finance and Economics ISSN 1450-2887 Issue 47

- Watts, R. and Zimmerman, J. (2013). Positive Accounting Theory. Englewood Cliffs, Prentice Hall, Inc.

- Welch, I. (2011). Two common problems in Capital Structure research: The financial debt-to asset ratio and issuing activity vs. Leverage changes”. International Review of Finance, 11 Crossref

- Zang, A. Y. (2007). Evidence on the Tradeoff between Real Manipulation and Accrual Manipulation”. Working Paper, University of Rochester. Crossref

- Zhang, H., (2002). Detecting earnings management: Evidence from rounding-up earnings per share”. Working Paper, University of Illinois, Chicago, MC/006.

- Zhang, R. (2006): “Cash Flow management, incentives, and market pricing”. Working Paper, Guanghua School of Management. Crossref

- Zagers, I. (2009). The effect of Leverage Increases on Real Earnings Management. Working Paper.

- Zamri, N., Abdul Rahman, R., Mohd and Isa, N. S. (2013). The impact of leverage on real earnings management. Procedia Economic and Finance. 7, 86-95. Crossref

{kind=link}