International Journal of Management Science and Business Administration

Volume 6, Issue 1, November 2019, Pages 7-12

The Significance of Derivatives in the Management of the Value of Non-Financial Enterprises in Poland on the Age of Financialization

DOI: 10.18775/ijmsba.1849-5664-5419.2014.61.1001

URL: http://dx.doi.org/10.18775/ijmsba.1849-5664-5419.2014.61.1001

Alina Rydzewska

Silesian University of Technology, Poland

Abstract: The turn of the 21st century is a period of the growing importance of finance in the global economy. The domination of the financial sphere about the real sphere is defined as financialization. The inflation of financial instruments, derivatives, in particular, is indicated among the symptoms of financialization. Financialization about companies is associated with the growing importance of financial motives in the decision-making processes of enterprises. The enlarging pressure of financial markets and investors forces transformations in the value management process. Companies raising capital from share issues are evaluated by investors (shareholders). In turn, management is entrusted to hired managers whose evaluation depends on the current results. To meet the requirements of the owners (shareholders), they stop taking into account the long-term development of a given undertaking and focus on achieving the required rate of return in the short term. Therefore, they limit their operational activities, and in particular long-term investment activities, in favour of short-term financial activities. They use derivatives as one of the forms of short-term profit generation. Their use is characterized by a relatively high level of risk resulting from the use of leverage in their construction. It also results in potential profits (or losses) many times higher than the capital employed. The purpose of this paper is to examine whether non-financial enterprises operating in Poland use derivatives in value management. The research was based on the analysis of indicators identifying the role of derivatives in the enterprise and determining their impact on the ROE ratio as a measure of value for shareholders. For this purpose, the financial statements of non-financial enterprises published in Poland by the Central Statistical Office for the years 2010-2017 were used.

Keywords: Inflation rates, Exchange rates, Interest rates, Stock market return volatility and monthly series

1. Introduction

Financialization is connected with the dominance of the financial sphere about the real sphere. The inflation of financial instruments, derivatives, in particular, is indicated among the symptoms of financialization [Ratajczak, 2012, p. 291]. Derivatives are financial assets whose prices depend on changes in the prices of underlying instruments (shares, bonds, stock indices, exchange rates, interest rates, etc.). Their original purpose was protection against risk, including FX risk. However, they quickly became a form of quick, profitable yet risky earning and in time, became speculative instruments. In the era of financialization, as a result of increased demand and the development of speculation on the derivatives market, dynamic growth of financial assets took place through the issue of new assets based on other assets. In addition to the quantitative increase in the value of derivatives, their development in terms of quality also took place. More and more financial instruments created by financial engineering have become more complicated and often illegible, especially for their buyers. Their multi-layered structure concerning revenue that depends on the price of another asset blurred the associated risk. This trend could be observed over the last quarter of a century, and it acquired exponential character in the years 2002-2008. The total nominal value of derivatives that were traded on the market in 1998 amounted to USD 72 billion, while in 2008, it was already USD 673 billion. In subsequent years, after the subprime crisis, their value fluctuated, exceeding USD 700 trillion in 2011 and 2013, while in 2018 it amounted to USD 544 trillion [BIS, https://www.bis.org/statistics/about_derivatives_ stats.htm?m=6%7C32%7C639].

Finalization is a challenge for contemporary managers. Financialization, when applied to non-financial entities, means the increase of importance of financial motives in the decision-making processes of enterprises. As a result of the transformations of the system of economic incentives and developmental patterns both in the economy and among business entities, concentration on quick earnings, on creating shareholder value occurred [Stockhammer, 2004, pp. 719-741]. For this purpose, managers use financial instruments to generate short-term profit, limiting operational and investment activity [Krippner, 2005, pp. 173-208, Orhangazi, 2008, pp. 863-886]. Such a possibility is offered to them by derivatives, which allow obtaining profits (or losses) many times higher than the capital employed, thanks to the use of the financial leverage in their structure.

The purpose of this paper is to examine whether non-financial enterprises operating in Poland use derivatives in building company value. The research was based on the analysis of indicators identifying the role of derivatives in the enterprise and determining their impact on the ROE ratio as a measure of value for shareholders. For this purpose, the financial statements of non-financial enterprises published in Poland by the Central Statistical Office for the years 2010-2017 were used.

2. Company Value Management in the Era of Financialization and Derivatives

Value management involves making strategic and operational decisions of investment, organizational, and financial nature that contribute to the growth of the company's value. According to the traditional approach, an increase in (the market) value of non-production companies is associated with the generation of long-term profit (income) from operational and investment activities. That is because core activity for such enterprises is the manufacture of goods (rendering services) and trade in goods. They generate revenues by selling them, which set off with the incurred costs constitute profits. The generated profit is the source of revenues for the owners and can be used to fund the investments. The investments determine the development of enterprise and larger earnings in the future. On the other hand, financial activity constitutes an additional source of revenues for financial investments when the enterprise has a surplus of non-allocated financial funds.

The financialization processes connected with the growing significance if the financial sector in the economy have led to transformations in the sphere of management and ownership. The companies obtaining their capital from financial markets as listed companies are assessed from the investors’ (shareholders) point of view).[Nawrocki, Szwajca, 2016, pp. 165-171.]. Owners-shareholders from the financial sphere treat their investments as one of periodical and alternative forms of funds allocation [Rydzewska, 2019, p. 282]. Their activities, especially the activities of institutional owners, are associated with the so-called impatient capital, which looks for the possibility to gain exceptional profits in a short period [Dore, 2002, pp. 115-121]. The company value management process is connected with the assessment of companies by the financial market. Company management is entrusted to managers whose position and remuneration depend on short-term results [Williams, 2000, pp.1-12]. One of the most frequently used indicators is the ROE indicator [Froud et al., 2000, pp. 80-110; Dembinski, 2011, p. 150 ]. Emphasis on the results well received by the financial markets means that managers move away from the stakeholder perspective and are guided towards the concept of management in the interest of the owners (the so-called shareholder perspective). [Palley, 2007, Jonek-Kowalska, I., Zieliński, M., 2017, pp. 1294-130]. In view of the above phenomena related to financialization, the management of company value is directed towards short-term financial results. Using the conditions of financialization, the companies look for sources that can ensure quick profits. Investments in financial instruments, derivatives, in particular, are one of the options.

Derivatives perform two fundamental functions in business trading, i.e., they hedge the risk of changes in the prices of underlying instruments and create the opportunity to achieve speculative profits. The first function is related to the fact that the entity wishing to avoid the risk of losses associated with adverse price fluctuations of the financial instrument (currency, interest rate, shares, etc.) through the purchase of a hedging derivative (contract, options) creates an insurance mechanism against future price changes. The use of hedging transactions involving derivatives allows the entrepreneur to predict the volume of flows (prices, margins) that will be realized in the future. Skilful use of hedging transactions can also affect the sales volume. When calculating sales prices based on quoting forward transactions, there is no need to assume a buffer for possible volatility, and the prices offered may be more competitive about other market participants. The hedging function of derivatives is mainly used in international trade. Thanks to the use of contracts or currency options, importers and exporters can insure themselves against FX fluctuations. The condition is a very precise knowledge of the functioning of the market on which the activity is conducted.

Derivatives are also a tool for achieving short-term (speculative) profits. Their attractiveness in generating quick and high profits is related to the possibility of using financial leverage, i.e., the potentiality of realisation disproportionately high earnings about the amount invested [Sopoćko, 2010, p. 134]. The capital invested in derivatives is usually a margin representing a small percentage of the nominal value of the purchased/sold instruments. However, it should be remembered that derivatives are high-risk instruments. The lever works in both directions. It can contribute to high profits, but also losses. Most transactions on derivatives are in fact, an obligation towards a financial institution that needs to be fulfilled. When we consider the importance of derivatives in managing the value of an enterprise in the era of finalization, their function as a speculative instrument is taken into account.

3. Research Methodology

The research method adopted to examine whether financialization processes influenced the value management of non-financial enterprises in Poland was the analysis of indicators built based on financial statements published by the Central Statistical Office for the years 2010-2017 [Financial instruments of non-financial enterprises, 2010-2017].

In order to assess the significance of derivative instruments in enterprises, indexes of derivatives' participation in the structure of assets/ sources of financing were used. In accordance with the legal regulations regarding accounting records [IAS 32, IAS 39, Accounting Act, Ordinance of the Minister of Finance on specific recognition principles, valuation methods, scope of disclosure and presentation of financial instruments], derivatives are recognized in financial statements at fair value, which the market price is most often considered to be. It should be noted that depending on the type of instrument and its characteristics, its presentation in records and financial statements may differ. And so, contracts (forward, future) result in the simultaneous creation of financial assets and financial liabilities. As at the balance sheet date, their value is adjusted to their market value. In contrast, options, depending on the side of the transaction, are recorded in two ways. If options are purchased, they are recognized as financial assets, and if they are offered for trading - as financial liabilities. Swap contracts are only valued for reporting purposes. The estimation of the fair value of the instrument may have a positive value (resulting in the financial asset recognition) or a negative one (resulting in the financial liability recognition) [Gmytrasiewicz, Karmańska, 2010, pp. 306-331].

Formula 1 shows the participation of derivatives in the balance sheet total.

This ratio expresses the share of derivatives in total assets or liabilities. The increase in the ratio indicates a greater involvement of free funds in derivatives as investments or as sources of financing.

Another indicator determining the role of derivatives in the functioning of non-financial enterprises is the ratio of participation of the result from operations on derivatives in the net financial result. This indicator is presented in Formula 2.

![]()

This indicator shows the share of profit (loss) generated as part of operations on derivatives in the net profit of the enterprise. The growth of it means an increase in the significance of income from operations related to derivatives in total income.

Due to time constraints of data on the result from operations on derivatives (until 2015), the ratio expressing the relation of the pre-tax financial result (gross) to the operating result (model 3) was adopted as a supplementary indicator.

![]()

This indicator shows the extent to which financial activities (including derivative transactions) affected the operating activity of the enterprise. When the indicator is greater than 1, it means that the enterprise generates profit from financial activities, which increases the operating result. The indicator lower than 1 shows that the result on financial operations is negative and absorbs profits generated from operating activities.

To assess the value of the enterprise (for shareholders), the ROE ratio was used, in accordance with the trends observed in practice among investors-shareholders. Its formula is as presented in Formula 4.

![]()

This indicator demonstrates the profitability of equity, i.e., how much net income each monetary union brings by engaging in the equity of a given enterprise. In general, the higher the ratio, the higher the profit value for the owners (shareholders).

4. Empirical Analysis

Empirical analysis concerning the significance of derivatives in the value management of a company was carried out for the period 2010-2017.

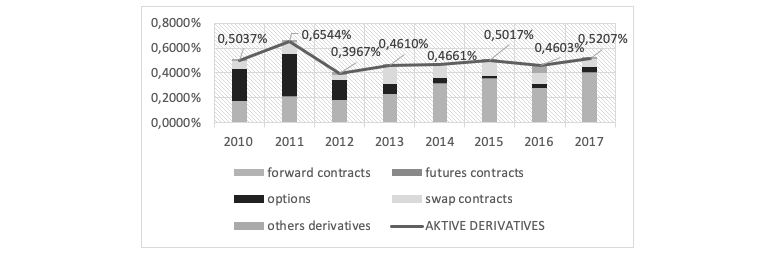

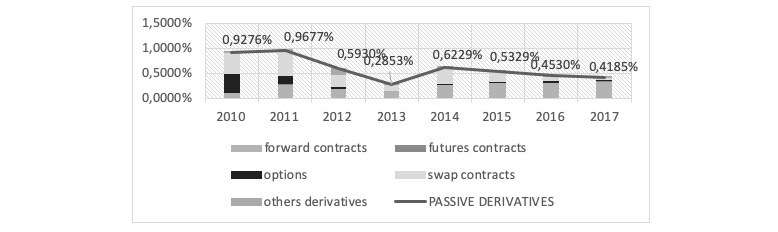

The indicators of the share of derivatives in the balance sheet total have been presented in two charts. Chart 1 presents the structure of active derivatives, while Chart 2 – the structure of passive derivatives.

Figure 1: The structure of active derivatives of non-financial enterprises in Poland in the years 2010-2017 (own work based on Financial instruments of non-financial enterprises, Central Statistical Office, Warsaw, 2010-2017

Examining the structure of derivatives in the balance sheet total of the Polish non-financial enterprises, it can be concluded that the share of derivatives in total assets/ liabilities is low– it does not exceed 1%. As far as active derivatives are concerned, their highest level was observed in 2011 and amounted to 0.65%. In the following years it decreased to approx. 0.5%. The share of passive derivatives exceeded 0.9% in the years 2010-2011. In subsequent years, it fell to 0.3% in 2013, and then it stalled at around 0.4%.

Figure 2: The structure of passive derivatives of non-financial enterprises in Poland in the years 2010-2017 (own work based on Financial instruments of non-financial enterprises, Central Statistical Office, Warsaw, 2010-2017)

Analyzing the types of derivatives, it can be observed that in 2011-2012, options were a dominant group within the assets (0.26% in 2010, 0.34% in 2011). Enterprises purchased options as a form of investment. On the passive side, their share in 2010 was 0.37%, and in 2011 it fell to 0.16%. Thus, a smaller group of enterprises issued options. On the other hand, in the initial period of analysis, swap contracts dominated within the liabilities (0.42% in 2010, 0.51% in 2011). It means that in the covered period, swaps caused a negative valuation in a greater number of non-financial enterprises. After 2013, forward contracts were the most frequently used derivatives. Both on the side of assets and liabilities, their level approximated 0.3%. A slightly higher value was on the asset side, which was associated with the valuation as at the balance sheet date.

Table 1: Indicators of the share of the result from operations on derivatives in the net financial result, the ratio gross result / operating result, ROE of non-financial enterprises in Poland in 2010-2017 (own work based on Financial instruments of non-financial enterprises, Central Statistical Office, Warsaw, 2010-2017)

Examining the significance of derivatives in management of the value of the polish enterprises, the effects of investing in derivatives, and the results achieved by the enterprise should be analyzed. When we analyse the profitability of derivatives based on the ratio of the result from operations on derivatives to the net financial result, it can be seen that it was at a low level of around 1%. The highest value was observed in 2013 and amounted to 1.39%. In contrast, in 2010, 2012, and 2015, its value was negative, while ROE was positive. It means that operations on derivatives hurt the profitability of equity. Due to the limited data on results from operations on derivatives for the years before 2015, the ratio of the gross financial result (before tax) to the operating result was additionally used. This ratio was lower than 1 in all years of the analysis (2010-2015). It means that the result from all financial operations (including derivatives) was negative and absorbed profits generated from operating activity. Thus, it negatively affected the ROE ratio, which had positive values in the same period.

5. Conclusion

The purpose of this paper was to examine whether non-financial enterprises operating in Poland use derivatives in value management.

Based on the conducted research, it should be said that derivatives did not contribute to the creation of the value of Polish enterprises (measured by ROE). The share of derivatives in the balance sheet total in 2010-2018 was at a low level and did not exceed 1%. What is more, the analysis of types of derivatives indicates that the forward contracts and foreign currency swaps are dominant. These are instruments with an individual character, and they perform mainly a hedging function, not a speculative one. However, the most important conclusions come from the analysis of profitability on derivatives. The ratio of the share of the result on financial operations in the net financial result was also low, not exceeding 1%. In the years 2010, 2012, and 2015, its value was negative, while ROE was positive. The additionally analyzed ratio of the gross financial result to the financial result from operating activity in the covered period was less than 1, which means that the result from operations on financial instruments (including derivatives) hurt the financial result and thus the ROE ratio. The research carried out concerns the period of the past eight years. Financialization is a developing phenomenon. Therefore, research into the discussed issues should be continued.

References

- Accounting Act. [Ustawa o rachunkowości z 29 września 1994 r. (Dz.U. z 2001 r. nr 149, poz. 1674 ze zm.)]

- Dembiński P. H. (2011), Finanse po zawale. od euforii finansowej do gospodarczego ładu, Studio Emka, Warszawa.

- Dore R. (2002), Stock Market Capitalism and Its Diffusion, New Political Economy, 2002, 1 (7).

- Financial instruments of non-financial enterprises, Central Statistical Office, Warsaw, 2010-2017. Retrieved 15.11.2019 from http://stat.gov.pl/obszary-tematyczne/podmioty-gospodarcze-wyniki-finansowe/

- Froud J., Haslam C, Johal S., Williams K. (2000), Shareholder value and financialisation; consultancy promises, management moves, Economy and Society, 29 (1). Crossref

- Gmytrasiewicz M., Karmańska A (2010), Rachunkowośc finansowa, Difin.

- International Accounting Standards 32, Financial Instruments: Presentation.

- International Accounting Standards 39, Financial Instruments: Recognition and Measurement.

- Jonek-Kowalska, I., Zieliński, M. (2017), CSR activities in the banking sector in Poland, Proceedings of the 29th International Business Information Management Association Conference - Education Excellence and Innovation Management through Vision 2020: From Regional Development Sustainability to Global Economic Growth.

- Krippner G.R. (2005), the financialization of the American economy, Socio-Economic Review, 3 (2). Crossref

- Nawrocki T. L., Szwajca D. (2016), the Concept of Corporate Reputation Assessment Model – the Stock Market Investors Perspective. [w:] Strategic Innovative Marketing, Kavoura A., Sakas D. P., Tomaras P. (eds.) Springer Proceedings in Business and Economics. Crossref

- Ordinance of the Minister of Finance on specific recognition principles, valuation methods, scope of disclosure and presentation of financial instruments [Rozporządzenie ministra finansów z 12 grudnia 2001 r. w sprawie szczegółowych zasad uznawania, metod wyceny, zakresu ujawniania i sposobu prezentacji instrumentów finansowych (Dz.U. z 2001 r. nr 149, poz. 1674 ze zm.)]

- Orhangazi O. (2008), Financialisation and capital accumulation in the non-financial corporate sector: A theoretical and empirical investigation on the US economy: 1973-2003, Cambridge Journal of Economics, 32 (6). Crossref

- Palley T.I. (2007), Financialization: What It Is and Why it Matters, The Levy Economics Institute and Economics for Democratic and Open Societies Washington, D.C, 2007, Working Paper Series, nr 525 przedsiebiorstwa-niefinansowe/instrumenty-finansowe-przedsiebiorstw-niefinansowych,20,3.html. Crossref

- Ratajczak M. (2012), Financialisation of the economy, Ekonomista (3).

- Retrieved 15.11.2019 from https://www.bis.org/statistics/about_derivatives_stats.htm?m=6%7C32%7C639.

- Rydzewska A. (2019), Financialization of Polish enterprises from the aspect of their size, 6th International Multidisciplinary Scientific Conference on Social Science & Arts, SGEM 2019, Conference Proceedings, Vol. 6, Modern Science, Issue 6, Vienna, Austria.

- Sopoćko A. (2010), Rynkowe instrumenty finansowe, PWN, Warszawa.

- Stockhammer E. (2004), Financialisation and the Slowdown of Accumulation, Cambridge Journal of Economics, 28 (5). Crossref

- Williams K. (2000), From Shareholder Value to Present-day Capitalism, Economy and Society, 29 (1). Crossref

{kind=link}